Recently one of our faithful readers, Natalie, emailed us to share a website she'd found. It's called Knock-Off Wood. Have you heard of it?

Let me tell you a little bit about it.

The creator, Ana White, is a furniture designer and builder. In her blog bio, she says this: "I'm just a stay at home Mom with expensive taste and no money. But money (or rather the lack of money) is not going to keep me from making our home comfortable, organized and stylish."

I'm sure there are many of us that can relate!

Without any formal training, she has learned how to look at retail furniture, then go home and duplicate it. Unbelievable! Her blog is a forum where she shares her designs FOR FREE, and lets other people share their building success stories.

I fell in love with her blog after moments of perusing, not only because she has everything organized by skill level, type of furniture, style of furniture, and many more, but mostly because all of her pieces are so so inexpensive. If you look at the "search plans by estimated cost," there isn't a category over $200. Can you imagine being able to build an RC Willey bed or a Pottery Barn armoire for less than $200??

I, personally, am not a builder, but her plans are so simple that even beginner carpenters (like me) could build a lot of these pieces. Each plan has a supply list, a cut list, a tool list, and then step by step instructions on how to build the furniture. With the help of the nice men at Home Depot who will cut your wood for you (and even though they have a sign that says $0.25/cut, they never charge me), you don't even need a saw!

This website is an amazing resource for people looking for inexpensive furniture. Yes, it takes some time and effort, but I think the price makes it worth your while. Plus, you'll have unbelievable bragging rights for the rest of your life.

The second I have a new house and room for some new furniture, I'm building myself this. Or maybe one of these. Or maybe I'll just make one of everything.

Jul 29, 2010

Jul 28, 2010

Small Savings: Homemade Stock (Janssen)

There are some common grocery items where the price doesn't phase me at all. Yogurt? No problem. Sugar? Got tons.

But for some reason, I find chicken broth absurdly expensive. Or filled with chemicals. Or both. When I'm making a recipe that calls for something like 7 cups of chicken broth, I am filled with horror.

You can make your own chicken stock by boiling chicken bones, but I rarely, if ever, buy chicken with bones in it, so this doesn't really solve my problem.

I do, however, buy a lot of vegetables and there are always parts of vegetables you don't really eat on their own (the tops of celery stalks, carrot peelings or tops, the ends of onions, broccoli stems, etc). And frankly, I don't really notice a difference between chicken broth and vegetable broth.

Over the course of a week or so, I put the leftover vegetables parts in a tupperware until I have a good little pile.

I toss it all in my stockpot, cover it with water, put in some bay leaves, garlic, salt and pepper, and let it simmer for a few hours. Then I cool it, strain out the vegetables, pour the broth in my ice cube molds, and put the frozen cubes in a big tupperware in the freezer.

Then, when I need it for a recipe, it costs me virtually nothing, even if the recipe requires a ludicrous amount of broth. Plus, I get to feel good about not having wasted my vegetables. Not to mention that it's not filled with weird ingredients.

But for some reason, I find chicken broth absurdly expensive. Or filled with chemicals. Or both. When I'm making a recipe that calls for something like 7 cups of chicken broth, I am filled with horror.

You can make your own chicken stock by boiling chicken bones, but I rarely, if ever, buy chicken with bones in it, so this doesn't really solve my problem.

I do, however, buy a lot of vegetables and there are always parts of vegetables you don't really eat on their own (the tops of celery stalks, carrot peelings or tops, the ends of onions, broccoli stems, etc). And frankly, I don't really notice a difference between chicken broth and vegetable broth.

Over the course of a week or so, I put the leftover vegetables parts in a tupperware until I have a good little pile.

I toss it all in my stockpot, cover it with water, put in some bay leaves, garlic, salt and pepper, and let it simmer for a few hours. Then I cool it, strain out the vegetables, pour the broth in my ice cube molds, and put the frozen cubes in a big tupperware in the freezer.

Then, when I need it for a recipe, it costs me virtually nothing, even if the recipe requires a ludicrous amount of broth. Plus, I get to feel good about not having wasted my vegetables. Not to mention that it's not filled with weird ingredients.

Share To:

Jul 27, 2010

What is a Mutual Fund? (Carole)

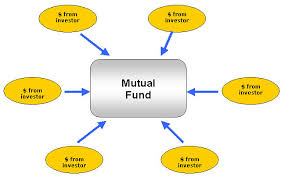

Sometimes we hear financial terms (maybe even use them ourselves) and yet don't really know what they mean. Maybe the term Mutual Fund falls into this category for you. I'm going to try explain what a Mutual Fund is in less than 200 words. Here we go. . .

*A Mutual Fund is a pool of money (millions and millions of dollars) from thousands of investors. Get it? You are all mutually funding this huge investment vehicle.

*These millions and millions of dollars are used to buy DIFFERENT types of stocks (or possibly bonds) within this one Mutual Fund. Your Mutual Fund can own stocks from stores, high tech companies, oil companies, banks. . .whatever businesses out there are selling stocks.

*These diverse stocks are carefully chosen by a Fund Manager. His or her job is to choose wisely and broadly so that if one segment of the financial world (say, the price of oil) goes down, chances are that a different segment of the financial world (say, the value of Wal-Mart stock) goes up. The Fund Manager's needs to make sure you own both kinds of stock, so your investment money is safe -- and hopefully earning interest. Actually their job is to make sure you own dozens of different kinds of stocks that can balance one another out, which greatly reduces your risk. With this kind of diversity, the chance that you will lose all of the money you (or any of the investors) have put into the fund, are very very small.

That's it. That's all a Mutual Fund is. You can purchase Mutual Funds that specialize in a particular philosophy or segment of society: Green Products and Technology, International Companies, U.S. only based companies, Christian Principles or just about any niche you can imagine. Mutual Funds are also divided into categories based on how risky the stocks are that the Fund owns. Your investor can help you determine how much of a gambler you really are as you choose your Mutual Funds.

The reason most small investors like Mutual Funds, is because they allow you to have a very diverse portfolio of investments with very little money invested. If you had $2,000 invested on your own in the stock market, you could probably only afford to buy a few stocks in a couple of companies. But in a Mutual Fund you will own parts of hundreds or thousands of different stocks.

Mutual Funds tend to be a much safer way to invest your hard-earned $$.

*A Mutual Fund is a pool of money (millions and millions of dollars) from thousands of investors. Get it? You are all mutually funding this huge investment vehicle.

*These millions and millions of dollars are used to buy DIFFERENT types of stocks (or possibly bonds) within this one Mutual Fund. Your Mutual Fund can own stocks from stores, high tech companies, oil companies, banks. . .whatever businesses out there are selling stocks.

*These diverse stocks are carefully chosen by a Fund Manager. His or her job is to choose wisely and broadly so that if one segment of the financial world (say, the price of oil) goes down, chances are that a different segment of the financial world (say, the value of Wal-Mart stock) goes up. The Fund Manager's needs to make sure you own both kinds of stock, so your investment money is safe -- and hopefully earning interest. Actually their job is to make sure you own dozens of different kinds of stocks that can balance one another out, which greatly reduces your risk. With this kind of diversity, the chance that you will lose all of the money you (or any of the investors) have put into the fund, are very very small.

That's it. That's all a Mutual Fund is. You can purchase Mutual Funds that specialize in a particular philosophy or segment of society: Green Products and Technology, International Companies, U.S. only based companies, Christian Principles or just about any niche you can imagine. Mutual Funds are also divided into categories based on how risky the stocks are that the Fund owns. Your investor can help you determine how much of a gambler you really are as you choose your Mutual Funds.

The reason most small investors like Mutual Funds, is because they allow you to have a very diverse portfolio of investments with very little money invested. If you had $2,000 invested on your own in the stock market, you could probably only afford to buy a few stocks in a couple of companies. But in a Mutual Fund you will own parts of hundreds or thousands of different stocks.

Mutual Funds tend to be a much safer way to invest your hard-earned $$.

Share To:

Jul 26, 2010

CSN Winner!

I can't tell you all how much I enjoyed hearing all the great ways you save money and stay on track financially, from big consistent things to small one-time savings. What a fun crowd you are.

The winner is Carly, who said "We are really good at sitting down every month and going over the last month and next month's budget together. It helps that we communicate and set goals and account. Likewise we are good at sitting down periodically (it was last night) and doing longer term goals."

Congratulations and thanks everyone for their participation!

The winner is Carly, who said "We are really good at sitting down every month and going over the last month and next month's budget together. It helps that we communicate and set goals and account. Likewise we are good at sitting down periodically (it was last night) and doing longer term goals."

Congratulations and thanks everyone for their participation!

Share To:

Jul 23, 2010

Born Today!

Janssen and baby girl. 7lbs 7 oz. Thought you might all enjoy knowing that we've added a new member to our frugal family .

Carole (Happy Grandmother!)

Share To:

Speaking of Food Storage (Merrick)

Look what I found...this is really helpful if you're looking to stock up on food storage.

You can switch out things that you won't eat, and you can buy items every other week, or once a month instead of every week, or you can buy the items in smaller increments. But this gives you a good idea of how much food you should have, and what types of food you should have (obviously this doesn't include water).

Like I mentioned in my previous post, buying small amounts each week, or every few weeks doesn't cost you much more on your grocery bill, but helps you slowly build up your supply of food.

Two Years of Food Storage

This is a list of food storage items to pick up at the store every week for one year. At the end of one year, you will have food storage for 2 people for 2 years!

Week 1: 6 lbs salt

Week 2: 5 cans cream of chicken soup

Week 3: 20 lbs sugar

Week 4: 8 cans tomato soup

Week 5: 50 lbs wheat

Week 6: 6 lbs macaroni

Week 7: 20 lbs sugar

Week 8: 8 cans tuna

Week 9: 61 lbs yeast

Week 10: 50 lbs wheat

Week 11: 8 cans tomato soup

Week 12: 20 lbs sugar

Week 13: 10 lbs powdered sugar

Week 14: 7 boxes macaroni and cheese

Week 15: 50 lbs wheat

Week 16: 5 cans cream of chicken soup

Week 17: 1 bottle 500 multivitamins

Week 18: 10 lbs powdered milk

Week 19: 5 cans cream of mushroom soup

Week 20: 50 lbs wheat

Week 21: 8 cans tomato soup

Week 22: 20 lbs sugar

Week 23: 8 cans tuna

Week 24: 6 lbs shortening

Week 25: 5 lbs honey

Week 26: 50 lbs wheat

Week 27: 10 lbs powdered milk

Week 28: 20 lbs sugar

Week 29: 5 lbs peanut butter

Week 30: 50 lbs wheat

Week 31: 7 boxes macaroni and cheese

Week 32: 10 lbs powdered milk

Week 33: 1 bottle 500 asprin or tylenol

Week 34: 5 cans cream of chicken soup

Week 35: 50 lbs of wheat

Week 36: 7 boxes macaroni and cheese

Week 37: 6 lbs of salt

Week 38: 20 lbs sugar

Week 39: 8 cans tomato soup

Week 40: 50 lbs of wheat

Week 41: 5 cans cream of chicken soup

Week 42: 20 lbs sugar

Week 43: 1 bottle 500 multivitamins

Week 44: 8 cans tuna

Week 45: 50 lbs wheat

Week 46: 6 lbs macaroni

Week 47: 20 lbs sugar

Week 48: 5 cans cream of mushroom soup

Week 49: 5 lbs of honey

Week 50: 20 lbs sugar

Week 51: 8 cans tomato soup

Week 52: 50 lbs wheat

You can switch out things that you won't eat, and you can buy items every other week, or once a month instead of every week, or you can buy the items in smaller increments. But this gives you a good idea of how much food you should have, and what types of food you should have (obviously this doesn't include water).

Like I mentioned in my previous post, buying small amounts each week, or every few weeks doesn't cost you much more on your grocery bill, but helps you slowly build up your supply of food.

Two Years of Food Storage

This is a list of food storage items to pick up at the store every week for one year. At the end of one year, you will have food storage for 2 people for 2 years!

Week 1: 6 lbs salt

Week 2: 5 cans cream of chicken soup

Week 3: 20 lbs sugar

Week 4: 8 cans tomato soup

Week 5: 50 lbs wheat

Week 6: 6 lbs macaroni

Week 7: 20 lbs sugar

Week 8: 8 cans tuna

Week 9: 61 lbs yeast

Week 10: 50 lbs wheat

Week 11: 8 cans tomato soup

Week 12: 20 lbs sugar

Week 13: 10 lbs powdered sugar

Week 14: 7 boxes macaroni and cheese

Week 15: 50 lbs wheat

Week 16: 5 cans cream of chicken soup

Week 17: 1 bottle 500 multivitamins

Week 18: 10 lbs powdered milk

Week 19: 5 cans cream of mushroom soup

Week 20: 50 lbs wheat

Week 21: 8 cans tomato soup

Week 22: 20 lbs sugar

Week 23: 8 cans tuna

Week 24: 6 lbs shortening

Week 25: 5 lbs honey

Week 26: 50 lbs wheat

Week 27: 10 lbs powdered milk

Week 28: 20 lbs sugar

Week 29: 5 lbs peanut butter

Week 30: 50 lbs wheat

Week 31: 7 boxes macaroni and cheese

Week 32: 10 lbs powdered milk

Week 33: 1 bottle 500 asprin or tylenol

Week 34: 5 cans cream of chicken soup

Week 35: 50 lbs of wheat

Week 36: 7 boxes macaroni and cheese

Week 37: 6 lbs of salt

Week 38: 20 lbs sugar

Week 39: 8 cans tomato soup

Week 40: 50 lbs of wheat

Week 41: 5 cans cream of chicken soup

Week 42: 20 lbs sugar

Week 43: 1 bottle 500 multivitamins

Week 44: 8 cans tuna

Week 45: 50 lbs wheat

Week 46: 6 lbs macaroni

Week 47: 20 lbs sugar

Week 48: 5 cans cream of mushroom soup

Week 49: 5 lbs of honey

Week 50: 20 lbs sugar

Week 51: 8 cans tomato soup

Week 52: 50 lbs wheat

Share To:

Jul 22, 2010

Small Savings: Unloved Bread Ends (Janssen)

I don't know about you, but I often get down to the last slice or two of bread and it's looking a little stale, or too thin, or it's the end piece and I don't really want to use it. I'd rather just move on to a new, whole loaf.

But throwing that bread away seems so wasteful, and I always imagine my dad cringing. Which means that I sometimes find myself with two or three almost empty bread bags in the back of my fridge.

Instead of throwing them away, I've found two ways to use them to avoid having to buy other products:

But throwing that bread away seems so wasteful, and I always imagine my dad cringing. Which means that I sometimes find myself with two or three almost empty bread bags in the back of my fridge.

Instead of throwing them away, I've found two ways to use them to avoid having to buy other products:

- I take the leftover slices of bread, toss them into the food processor and blend them until they are tiny little crumbs. I then dump the whole thing into a large ziplock back and stick it in the freezer. Whenever I have a recipe that calls for breadcrumbs, there they are, ready and waiting (and homemade!).

- I make my own croutons. I take a slice of bread (the end works just as well as a regular slice of bread) and cut it into strips and then squares (I'd say about 25 squares per slice - 5 rows by 5 rows). I dump it into a bowl, mix in a little olive oil, salt, pepper, and dried herbs (basil, oregano or an Italian Mix is my standard), then toss it on a baking sheet and cook them at 350 for about 15 minutes, or until they are toasty and brown. Stir them occasionally to keep from burning. These last quite well in the fridge, I've found, staying crunchy for about a week after I make them. Bonus, you save money by not having to go to the dentist to get your broken tooth fixed - am I the only one who fears for my teeth whenever I bite into a store-bought crouton?

Share To:

Jul 21, 2010

The Magic of Compound Interest (Carole)

When you are investing money, there are two basic types of interest your money can earn: Simple Interest and Compound Interest.

Quickly, let's look at the difference between these.

Add this interest earned to your original $10,000

The formula is a bit complex and hard for me to type out, but you can look it up here if you just really need to see it for yourself.

Monthly Interest = $27,126.40

Yearly Interest = $26,532.98

The longer your money is invested the more interest you'll earn. Your same $10,000 at 5% for 30 years turns into $43,219.42 Same money, same interest for 40 years is $70,399.89

The higher your interest rate, the more interest you'll earn. Your same $10,000 at 10% for 20 years will become $67,275.00

Combine longer time and higher interest and it starts to get really fun:

$10,000 at 10% for 30 years = $174,494.02

$10,000 at 10% for 40 years = $452,592.56

$10,000 at 12% for 20 years = $96,462.93

$10,000 at 12% for 30 years = $299,599.22

$10,000 at 12% for 40 years = $930,509.70 (yep, nearly a million $)

Imagine if you could scrape together only $10,000 by age 20 and find a good mutual fund that paid 12% interest (not that difficult really) and just LEFT YOUR MONEY THERE until you were 65 years old, you would have $1,639,876.04 That's without you ever adding one more cent of principal to this investment. The sooner you can get investing in something earning a decent interest rate, the better off you will be at retirement.

That is magic. If you want to work some magic yourself, here is a compound interest calculator. I'll warn you -- it's addictive!

P.S. Your mortgage (or car payment, student loan, credit card bill. . .) works on a compound interest formula in your lender's favor. That is why you often end up paying 3 times the cost of your house by the time your loan is completed.

Quickly, let's look at the difference between these.

Simple Interest

(Interest is only calculated on the money you have invested):

If you invest $10,000 (your principal) at 5% interest for 20 years:$10,000 x 5% x 20 years = $10,000 (interest earned)

$10,000 + $10,000 = $20,000

Compound Interest

(Interest is calculated on your invested money PLUS your previously earned interest):

If you invest $10,000 (your principal) at 5% interest for 20 years with compound interest you'll end up with $26,532.98 . The formula is a bit complex and hard for me to type out, but you can look it up here if you just really need to see it for yourself.

In addition:

The more often your compound is calculated (daily, monthly, yearly) the more interest you will earn. Daily Interest = $27,180.96Monthly Interest = $27,126.40

Yearly Interest = $26,532.98

The longer your money is invested the more interest you'll earn. Your same $10,000 at 5% for 30 years turns into $43,219.42 Same money, same interest for 40 years is $70,399.89

The higher your interest rate, the more interest you'll earn. Your same $10,000 at 10% for 20 years will become $67,275.00

Combine longer time and higher interest and it starts to get really fun:

$10,000 at 10% for 30 years = $174,494.02

$10,000 at 10% for 40 years = $452,592.56

$10,000 at 12% for 20 years = $96,462.93

$10,000 at 12% for 30 years = $299,599.22

$10,000 at 12% for 40 years = $930,509.70 (yep, nearly a million $)

Imagine if you could scrape together only $10,000 by age 20 and find a good mutual fund that paid 12% interest (not that difficult really) and just LEFT YOUR MONEY THERE until you were 65 years old, you would have $1,639,876.04 That's without you ever adding one more cent of principal to this investment. The sooner you can get investing in something earning a decent interest rate, the better off you will be at retirement.

That is magic. If you want to work some magic yourself, here is a compound interest calculator. I'll warn you -- it's addictive!

P.S. Your mortgage (or car payment, student loan, credit card bill. . .) works on a compound interest formula in your lender's favor. That is why you often end up paying 3 times the cost of your house by the time your loan is completed.

Share To:

Jul 20, 2010

CSN Giveaway

While we all sit around waiting for my baby to arrive (you are all sitting around waiting for my baby to arrive, aren't you?), we thought it'd be fun to do another giveaway.

We're giving away a $50 gift certificate to any of the 200 online CSN stores. They sell, almost literally, everything you can possibly imagine.

Since I'll be moving to a bigger apartment soon (expect some "moving without selling your firstborn child to cover the expenses" posts soon), with a kitchen where the fridge can open all the way, I may be spending a little too much time looking at all the fun dishes that I'll actually have room to store in my new kitchen (no matter what else gets the axe, my beloved Le Creuset dishes from my great-aunt at our wedding will be making the trip back to Texas with me).

Frankly, I don't even KNOW what I would choose if I won, because there are so many options. Baby furniture might also be toward the top of the list for me. . .

If you win, you can use your $50 toward any last thing you desire and the options are many.

To enter, leave a comment telling us something you do well financially - we want to hear about your successes! We'll randomly choose a winner over the weekend and announce on Monday!

This is only open to residents of the US and Canada. This contest is sponsored by CSN stores.

We're giving away a $50 gift certificate to any of the 200 online CSN stores. They sell, almost literally, everything you can possibly imagine.

Since I'll be moving to a bigger apartment soon (expect some "moving without selling your firstborn child to cover the expenses" posts soon), with a kitchen where the fridge can open all the way, I may be spending a little too much time looking at all the fun dishes that I'll actually have room to store in my new kitchen (no matter what else gets the axe, my beloved Le Creuset dishes from my great-aunt at our wedding will be making the trip back to Texas with me).

Frankly, I don't even KNOW what I would choose if I won, because there are so many options. Baby furniture might also be toward the top of the list for me. . .

If you win, you can use your $50 toward any last thing you desire and the options are many.

To enter, leave a comment telling us something you do well financially - we want to hear about your successes! We'll randomly choose a winner over the weekend and announce on Monday!

This is only open to residents of the US and Canada. This contest is sponsored by CSN stores.

Share To:

Jul 19, 2010

Food Storage (Merrick)

When we did our 100th Post Giveaway, someone commented about food storage, and it got me thinking. I grew up in a home where my dad was a huge food storage guy. We drank powdered milk, made wheat bread from canned wheat, and froze large quantities of fruit from the trees in our garden. But growing up this way isn't the only reason I'm an advocate of food storage; here are a few other reasons:

1. Having food storage can decrease your weekly purchases at the store. Food storage doesn't have to be, and shouldn't be, only lentil beans and potato pearls -- it should be things that you want to eat and will eat. It's the "overbuyer" concept. When I make up my weekly menu, I go through my list of ingredients and see what I need and what I already have. If I purchased extra canned tomatoes or cream of chicken soup when they were on sale a few weeks back, that is one less thing I have to buy this week. Or if my budget is tight on a particular week, I can look in my pantry and build my menu around pasta or canned green chilies that I already have. If you're a couponer, use those coupons or wait for the big sales, and stock up on items you know you will use. Then when you go to make your grocery list, you will already have half of the ingredients.

2. In this economy with frequent layoffs and salary decreases, it's nice to have a food cushion. I know several people who have lost their jobs and have been able to live very cheaply because they can live off their food storage for a few weeks or months.

3. With all of the earthquakes, hurricanes, and other natural disasters that have hit so many people recently, there is no doubt in my mind that a little extra food in your pantry is a good thing, just in case you can't get to the grocery store for a few days.

Now obviously the nature of this blog is saving money, and building food storage costs money. But as I mentioned above, wait for the sales (especially caselot sales), use coupons, or just buy two cans of beans instead of one each week, and soon you'll be on your way to a nice supply of food without breaking the bank.

1. Having food storage can decrease your weekly purchases at the store. Food storage doesn't have to be, and shouldn't be, only lentil beans and potato pearls -- it should be things that you want to eat and will eat. It's the "overbuyer" concept. When I make up my weekly menu, I go through my list of ingredients and see what I need and what I already have. If I purchased extra canned tomatoes or cream of chicken soup when they were on sale a few weeks back, that is one less thing I have to buy this week. Or if my budget is tight on a particular week, I can look in my pantry and build my menu around pasta or canned green chilies that I already have. If you're a couponer, use those coupons or wait for the big sales, and stock up on items you know you will use. Then when you go to make your grocery list, you will already have half of the ingredients.

2. In this economy with frequent layoffs and salary decreases, it's nice to have a food cushion. I know several people who have lost their jobs and have been able to live very cheaply because they can live off their food storage for a few weeks or months.

3. With all of the earthquakes, hurricanes, and other natural disasters that have hit so many people recently, there is no doubt in my mind that a little extra food in your pantry is a good thing, just in case you can't get to the grocery store for a few days.

Now obviously the nature of this blog is saving money, and building food storage costs money. But as I mentioned above, wait for the sales (especially caselot sales), use coupons, or just buy two cans of beans instead of one each week, and soon you'll be on your way to a nice supply of food without breaking the bank.

Share To:

Jul 16, 2010

Small Savings: Printing (Janssen)

When you're trying to live frugally, you can save on big-ticket items (a car, a house, a vacation, etc) or on smaller items (groceries, clothing, eating out, etc).

The savings you'll see if you buy a less-expensive car is far more than you'll probably see at the grocery store (I hope - maybe you buy really expensive groceries), but you'll probably go to the grocery store hundreds of times for every one car purchase, which means the savings you can get at the grocery store, while only a few dollars a time, can really add up over time.

One of the places I save a little money is with my home printer. We're not talking hundreds of dollars of savings here, but it is a place where we can cut costs a little bit with no real effort on our parts. We do this in two ways:

1) We realized last fall that 99% of our printing is done for things that don't require any particularly nice paper. It's just directions from Google Maps or grocery coupons or boarding passes for an airplane trip. Instead of buying packs of paper for a few dollars at Wal-Mart or the grocery store, we started hoarding all the paper that entered our house that was blank on one side. It became immediately obvious how MUCH paper we got. A calendar from church, a credit card offer in the mail, a letter informing us what precint to vote in. And then, we started bringing some home from work - the notices I got at school alone filled up our printer tray in a matter of days.

The grocery store doesn't care if my coupons have the date of the next PTA luncheon on the back. I can get to my destination just fine if my directions are printed on the back of my privacy policy notification from the bank.

2) As I said above, we realized that our printing rarely needed to be high quality. Printer ink is fairly expensive, so we hate to waste it. We went on to our computer settings and changed the automatic mode for our printer to "Fast Draft," rather than high-quality. The quality is still perfectly fine - I have no problem reading anything and it's sharp enough for the scanners to read the barcodes on my grocery coupons - but it uses a fraction of the ink and, bonus, prints FAR faster and your paper isn't warped from all that ink. Win-win.

I'm certainly not going on a cruise with these savings, but it's less trips to the store and less money out of my wallet.

The savings you'll see if you buy a less-expensive car is far more than you'll probably see at the grocery store (I hope - maybe you buy really expensive groceries), but you'll probably go to the grocery store hundreds of times for every one car purchase, which means the savings you can get at the grocery store, while only a few dollars a time, can really add up over time.

One of the places I save a little money is with my home printer. We're not talking hundreds of dollars of savings here, but it is a place where we can cut costs a little bit with no real effort on our parts. We do this in two ways:

1) We realized last fall that 99% of our printing is done for things that don't require any particularly nice paper. It's just directions from Google Maps or grocery coupons or boarding passes for an airplane trip. Instead of buying packs of paper for a few dollars at Wal-Mart or the grocery store, we started hoarding all the paper that entered our house that was blank on one side. It became immediately obvious how MUCH paper we got. A calendar from church, a credit card offer in the mail, a letter informing us what precint to vote in. And then, we started bringing some home from work - the notices I got at school alone filled up our printer tray in a matter of days.

The grocery store doesn't care if my coupons have the date of the next PTA luncheon on the back. I can get to my destination just fine if my directions are printed on the back of my privacy policy notification from the bank.

2) As I said above, we realized that our printing rarely needed to be high quality. Printer ink is fairly expensive, so we hate to waste it. We went on to our computer settings and changed the automatic mode for our printer to "Fast Draft," rather than high-quality. The quality is still perfectly fine - I have no problem reading anything and it's sharp enough for the scanners to read the barcodes on my grocery coupons - but it uses a fraction of the ink and, bonus, prints FAR faster and your paper isn't warped from all that ink. Win-win.

I'm certainly not going on a cruise with these savings, but it's less trips to the store and less money out of my wallet.

Share To:

Jul 15, 2010

Are You an Underbuyer or an Overbuyer? (Carole)

Even though Gretchen is a Yale trained lawyer (whoa!), she is also a pretty ordinary wife with two little girls. One day she came to the realization that even though "the days were long -- the years were short" and she was not really enjoying her daily life as much as she thought she should! You too?? After tons and tons of some pretty highbrow (and some lowbrow) reading, she embarked on a year-long "project" to find more happiness in her daily life. I won't give away her many many insights (told in a very readable style), but I will share one interesting concept relating to money that you might find useful from Chapter 7. Here's what she has to say, When I began to pay attention to people's relationship to money, I recognized two different approaches to buying: 'underbuying' and 'overbuying.' I am an underbuyer, I delay making purchases or buy as little as possible. . .I often consider buying an item, then decide, 'I'll get this some other time' or 'Maybe we don't really need this.' As an underbuyer, I often feel stressed because I don't have the things I need. I make a lot of late-night runs to the drugstore. I'm surrounded with things that are shabby, don't really work, or aren't exactly suitable.

She goes on to say, I gaze in wonder at the antics of my overbuyer friends. Overbuyers often lay in huge supplies of slow-use things like shampoo or cough medicine. They make a lot of purchases before they go on a trip or celebrate a holiday. They throw things away -- milk, medicine, even cans of soup -- because they've hit their expiration date. Like me, overbuyers feel stressed. They're oppressed by the . . . the clutter and waste often created by their overbuying.

Gretchen eventually recognizes that there must be a happy medium and that it probably lives more in the camp of the Overbuyer: I knew that I'd be happier if I made a mindful effort to thwart my underbuying impulse and instead worked to buy what I needed. For instance, I ended my just-in-time policy for restocking toilet paper. . .As Samuel Johnson remarked, 'To live in perpetual want of little things is a state, not indeed of torture, but of constant vexation. . . I realized that the paradoxical consequence of being an underbuyer was that I had to shop MORE OFTEN, while buying extras meant fewer trips to the cash register. I bought batteries, Band-Aids, lightbulbs, diapers -- things I knew we would need eventually.

Do you recognize yourself in any of this?? Are you an Overbuyer or an Underbuyer?? I have been a life-long sad, sniveling underbuyer -- just ask my girls. Constantly out of vacuum bags, light bulbs, tooth paste, pepperoni, chocolate chips (well, I might be short of this last one for a very different reason than not buying them). And the list goes on and on. On the other hand, living in a galaxy far far away, I have a lovely friend who is a very wise Overbuyer. She keeps an entire box of paper (filled with a dozen reams!) nestled safely near her printer. She purchases charming birthday cards 20-30 at a time and even has ten spare deodorants in her bathroom closet! She is prepared, prepared, prepared -- and smells good too! I've always wanted to be like her, but could never quite figure out before what the difference was between us. Mystery solved.

I'd love to hear how you buy and if it really makes you happy.

Share To:

Jul 14, 2010

Multiple Streams of Income

For the first year and a half of our marriage, I was still in school finishing up my bachelor's degree. Although Philip was working full time, his starting salary was somewhat small, and with the cost of school, plus a mortgage, our savings was doing anything but increasing.

Once I graduated, I immediately began a full time job. The difference in our bank account was unbelievable. With both of us working, we were suddenly saving a huge amount of money, and happily watching our bank account grow for the first time in months.

But we didn't stop there. We realized the value of multiple streams of income, and since then we have continually been on the lookout for extra income opportunities. For example, last summer I made and sold many embellished t-shirts. We frequently go through our house and find unwanted or duplicate items that we can sell on craigslist or at Plato's Closet. I have also made and sold headbands, clips, and hair ties.

Now, since I no longer have a job because I stay at home with my baby, I do commission artwork, and recently began teaching children's art lessons, which brings in quite a bit of extra cash.

Already having a job, or being a full-time mom shouldn't stop you from finding other methods of income, because every bit makes a difference.

If you sit down and think about it, I'm sure you can come up with something simple and not too time consuming that you could do to earn extra money. You'll be amazed at the difference even $10 a week can make to your bank account.

Any great ideas??

Once I graduated, I immediately began a full time job. The difference in our bank account was unbelievable. With both of us working, we were suddenly saving a huge amount of money, and happily watching our bank account grow for the first time in months.

But we didn't stop there. We realized the value of multiple streams of income, and since then we have continually been on the lookout for extra income opportunities. For example, last summer I made and sold many embellished t-shirts. We frequently go through our house and find unwanted or duplicate items that we can sell on craigslist or at Plato's Closet. I have also made and sold headbands, clips, and hair ties.

Now, since I no longer have a job because I stay at home with my baby, I do commission artwork, and recently began teaching children's art lessons, which brings in quite a bit of extra cash.

Already having a job, or being a full-time mom shouldn't stop you from finding other methods of income, because every bit makes a difference.

If you sit down and think about it, I'm sure you can come up with something simple and not too time consuming that you could do to earn extra money. You'll be amazed at the difference even $10 a week can make to your bank account.

Any great ideas??

Share To:

Jul 13, 2010

Financial Goals (Janssen)

Two months ago, my husband and I paid off the last of our student loans, making us completely debt-free. It was glorious.

Once those were gone, though, we had to figure out what our new financial goals were. This was a little tricky because now instead of having one single-minded purpose for any extra money, we had so many categories we could consider - investing, emergency funds, vacations, a new baby (that makes it sound like we are saving to buy a baby. . . ), cars, etc.

We sat down together, looked over our finances and our budget and decided that our priorities were the following three:

Once those were gone, though, we had to figure out what our new financial goals were. This was a little tricky because now instead of having one single-minded purpose for any extra money, we had so many categories we could consider - investing, emergency funds, vacations, a new baby (that makes it sound like we are saving to buy a baby. . . ), cars, etc.

We sat down together, looked over our finances and our budget and decided that our priorities were the following three:

- A fully-funded emergency fund. Following Dave Ramsey's steps, we had previously had an emergency fund of $1000 before we began pounding away at our student loans. Once you're done with your debt, however, he recommends an emergency fund that could support your family for 3-6 months. We reviewed our budget and decided what that amount was for us and started working away at it as quickly as we could. The good thing about this goal is that it has a finish line - once we got that dollar amount in the account (actually, we have it spread out over several accounts at different banks), we could just leave it and move on to our next goal.

- Long-term investing. We significantly increased the amount of money we contribute into my husband's 401(k). Because time is on our side at this point, we wanted to take advantage of that, as well as the match that his company provides.

- A down payment fund. We currently are renters and probably will continue to be for the next several years, as we don't want to buy another house until we are certain we will stay in it for at least five or more years (we owned a house in Texas for three years and even after selling it for more than we paid for it, we still would have come out ahead if we'd continued to rent for those years - a house is a money pit). Our goal is to have a down payment of 20% since this would allow us to avoid paying mortgage insurance. We have a fairly good idea of how much the kind of house in the locations we're considering would cost us, so while we don't have as solid a number as we do for our emergency fund, it's a pretty accurate ballpark figure, I think.

Share To:

Jul 12, 2010

What is an IRA? (Carole)

You probably already know that IRA stands for Individual Retirement Account.

It is the U.S. Government's way to encourage each citizen to save up to $5,000/year (or $6,000/year if you are 50 years old and older) with some pretty nice tax benefits. This means a married couple can save up to $10,000/year (or $12,000 if you're both 50 or older).

There are two types of IRAs. Traditional and Roth. They are quite different. Here are the basic concepts of each.

* Your contribution is NOT tax deductible, but ALL the principal and interest earnings are tax free when you withdraw them after age 59-1/2.

* You can withdraw your principal (the money you actually invested in the Roth IRA) at any age with no penalty. But you will pay penalties if you withdraw any of your interest earnings before age 59-1/2

* Your Roth IRA money can be invested in almost anything: stocks, bonds, CDs, investment property. . . through a bank or brokerage.

* Contributions ARE tax deductible. However, taxes (on principal and interest earned) will be charged when you begin to withdraw your money.

* You cannot withdraw any of your contribution or interest earned until age 59-1/2. You do not have to withdraw at that age, but MUST begin withdrawing by age 70-1/2. If you withdraw your money before you are 59-1/2 there is at least a 10% penalty. Ouch.

* Again, your Traditional IRA can be invested in almost anything: stocks, bonds, CDs, investment property. . . through a bank or brokerage.

To max out your yearly contribution would be a monthly investment of $416.67 per person (or $500 per person/month age 50 and older). However, your contributions can be made in any increment at any time, and you do not have to reach the $5,000 limit.

$10,000/year savings might not sound like it will ever amount to much, but if you can consistently put that away in either kind of IRA from age 40 until you retire at age 65, you'll have over $1,000,000. Just think how much you'll have if you start investing in your 20's!!! The earlier you start saving any amount in an IRA, the more money you'll have at retirement -- remember, compound interest is your very best friend over the long haul.

It is the U.S. Government's way to encourage each citizen to save up to $5,000/year (or $6,000/year if you are 50 years old and older) with some pretty nice tax benefits. This means a married couple can save up to $10,000/year (or $12,000 if you're both 50 or older).

There are two types of IRAs. Traditional and Roth. They are quite different. Here are the basic concepts of each.

Roth IRA

* If you file your taxes singly, you have to earn $120,000 or less that year to invest in a Roth IRA. If you are married and filing jointly, you have to have a combined income of $177,000 or less for the year. These amounts change nearly every year, so check with your investor for the current limits. In fact, I found various $ limits mentioned for 2010, but the above amounts seemed to be the most accurate. Investing through a government plan is a bit confusing! A good banker or broker will easily navigate you through it all.* Your contribution is NOT tax deductible, but ALL the principal and interest earnings are tax free when you withdraw them after age 59-1/2.

* You can withdraw your principal (the money you actually invested in the Roth IRA) at any age with no penalty. But you will pay penalties if you withdraw any of your interest earnings before age 59-1/2

* Your Roth IRA money can be invested in almost anything: stocks, bonds, CDs, investment property. . . through a bank or brokerage.

Traditional IRA

* There is not an income requirement to invest in a Traditional IRA.

* Contributions ARE tax deductible. However, taxes (on principal and interest earned) will be charged when you begin to withdraw your money.

* You cannot withdraw any of your contribution or interest earned until age 59-1/2. You do not have to withdraw at that age, but MUST begin withdrawing by age 70-1/2. If you withdraw your money before you are 59-1/2 there is at least a 10% penalty. Ouch.

* Again, your Traditional IRA can be invested in almost anything: stocks, bonds, CDs, investment property. . . through a bank or brokerage.

To max out your yearly contribution would be a monthly investment of $416.67 per person (or $500 per person/month age 50 and older). However, your contributions can be made in any increment at any time, and you do not have to reach the $5,000 limit.

$10,000/year savings might not sound like it will ever amount to much, but if you can consistently put that away in either kind of IRA from age 40 until you retire at age 65, you'll have over $1,000,000. Just think how much you'll have if you start investing in your 20's!!! The earlier you start saving any amount in an IRA, the more money you'll have at retirement -- remember, compound interest is your very best friend over the long haul.

Share To:

Jul 9, 2010

Frugal Shopping (Merrick)

If you're anything like me, sale racks lure you in. I often find myself in Old Navy and being tempted to buy items only because they're $5.

Because I know myself and know that I will do this, and then end up with items that I don't love, I have come up with a few shopping guidelines. Now every time I take an item off the rack, I ask myself these three questions:

1. Do I love it?

2. Will I wear it?

3. Does it fit in with the style of my current wardrobe?

Now, I still occasionally buy things that I don't end up loving, but with these guidelines I buy more things that I really love and will wear. Being frugal is not just about buying a $5 skirt; being frugal is spending your money on something that you'll actually wear. Think about it as price per wearing. A five dollar skirt that you never wear will remain five dollars. The price per wearing for a twenty dollar skirt that you wear once a week will soon cost only a few cents.

So the next time a sale rack lures you in, think about these three questions and make sure you're spending your money on something that you actually want and really love. Your wallet and closet space will thank you.

Because I know myself and know that I will do this, and then end up with items that I don't love, I have come up with a few shopping guidelines. Now every time I take an item off the rack, I ask myself these three questions:

1. Do I love it?

2. Will I wear it?

3. Does it fit in with the style of my current wardrobe?

Now, I still occasionally buy things that I don't end up loving, but with these guidelines I buy more things that I really love and will wear. Being frugal is not just about buying a $5 skirt; being frugal is spending your money on something that you'll actually wear. Think about it as price per wearing. A five dollar skirt that you never wear will remain five dollars. The price per wearing for a twenty dollar skirt that you wear once a week will soon cost only a few cents.

So the next time a sale rack lures you in, think about these three questions and make sure you're spending your money on something that you actually want and really love. Your wallet and closet space will thank you.

Share To:

Jul 7, 2010

Saving Money on the Nursery- Crib Bedding (Guest Post by Kayla)

This post is written by Kayla, who had the good sense to have two babies before Janssen had any so that she could pass along all her wisdom. She is also the queen of the homemade gift and her blog is full of pictures of darling items that will make you wish you lived next door.

What I have to say will either be rather upsetting or a huge relief to all the first time expectant mothers out there:

You do not need that darling fancy pants $300 crib bedding.

Picking out the crib bedding is like a motherhood rite of passage, something many of us spend hours agonizing over. I came thisclose to spending $250 on seriously awesome pirate bedding for my first son before I did some research and realized my money would be better spent elsewhere.

Crib bedding usually consists of the following:

A quick search at Target.com reveals that a standard fitted crib sheet can be had for $8-$10. When my first son was born I bought two white fitted sheets from Target for less than $20 and 2.5 years later they are still going strong. If you're the DIY type or want to use a funner (my Google spell check says "funner" is totally a word) fabric, here is a tutorial for making your own.

If you still need bumpers (and we did), there are a lot of safe, affordable options out there. While I was pregnant I really wanted these breathable bumpers but at the time they only had yellow gingham and I have my standards. Now there are a whole bunch more colors available and, at $23, they are quite affordable.

We ended up with the Kompisar crib bumper pad from Ikea. It fits the AAP recommendation of "thin, firm, well secured, and not 'pillow-like'" and, at $12.99, the price couldn't be beat. We put them on when Wes started scootching in his sleep and catching his legs in the bars and we took them off as soon as he was old enough to extricate himself.

So my crib bedding cost all of $33, leaving me lots of room left in my budget left for fun things like art, books and a bookcase, and fabric for re-covering my glider (a piece of furniture which, incidentally, I shouldn't have bothered spending money on, but that's another post altogether. Live and learn!).

What I have to say will either be rather upsetting or a huge relief to all the first time expectant mothers out there:

You do not need that darling fancy pants $300 crib bedding.

Picking out the crib bedding is like a motherhood rite of passage, something many of us spend hours agonizing over. I came thisclose to spending $250 on seriously awesome pirate bedding for my first son before I did some research and realized my money would be better spent elsewhere.

Crib bedding usually consists of the following:

- Quilt

- Crib Skirt

- Bumper

- Fitted sheet

- You should not use the quilt in the crib. Period. It is a suffocation hazard. You could get creative and hang it on the wall or something, but you are not supposed to put it over your baby (if you're concerned about keeping your baby warm this article from Baby Center has some good suggestions).

- Crib skirts are generally of the proper length to be used while the crib mattress is in the upper position but are too long to be used when you have to drop the mattress, around 5-8 months (although some skirts work in both positions).

- There is some debate over the necessity of crib bumpers but the new AAP recommendation is that soft, pillowy bumpers not be used. There is the possibility of the bumper covering a child's nose and mouth and causing suffocation, but there is also the possibility of something called "rebreathing," which is when soft bedding or other items in the baby's sleeping area trap carbon dioxide around the baby's face. It is speculated that this phenomenon is the cause behind a fair number of SIDS deaths. Plus, those fancy bumpers tend to be sturdier and thus become very handy step stools when your little Precious decides his crib is boring and he'd rather get down to the floor and play with an electrical outlet.

A quick search at Target.com reveals that a standard fitted crib sheet can be had for $8-$10. When my first son was born I bought two white fitted sheets from Target for less than $20 and 2.5 years later they are still going strong. If you're the DIY type or want to use a funner (my Google spell check says "funner" is totally a word) fabric, here is a tutorial for making your own.

If you still need bumpers (and we did), there are a lot of safe, affordable options out there. While I was pregnant I really wanted these breathable bumpers but at the time they only had yellow gingham and I have my standards. Now there are a whole bunch more colors available and, at $23, they are quite affordable.

We ended up with the Kompisar crib bumper pad from Ikea. It fits the AAP recommendation of "thin, firm, well secured, and not 'pillow-like'" and, at $12.99, the price couldn't be beat. We put them on when Wes started scootching in his sleep and catching his legs in the bars and we took them off as soon as he was old enough to extricate himself.

So my crib bedding cost all of $33, leaving me lots of room left in my budget left for fun things like art, books and a bookcase, and fabric for re-covering my glider (a piece of furniture which, incidentally, I shouldn't have bothered spending money on, but that's another post altogether. Live and learn!).

Share To:

Jul 6, 2010

June Savings Winner

You may remember that waaaaay back at the end of May, when we announced we were going to do a weekly round up of savings, we said there would be a prize for one of the people who participated all four weeks. We have another copy of Dave Ramsey's book The Total Money Makeover to give away.

And the winner is. . . . .Preethi!!!

Here were her contributions each week:

Week 1

Here were her contributions each week:

Week 1

- Bought food at the grocery store for our beach vacation instead of eating out. Because we were the last ones to leave, we ended up bringing home nearly as much in leftover supplies.

- Recalculated budget for the summer, including putting all of my summer internship salary toward student loans.

- Researched and found a great deal to replace our carpeting.

- Found my husband two all-wool suits from Macy's (he wears suits every day to work) for $60 each, marked down from an original of $450 each.

- Asked for and received a price adjustment for a purchase several days prior, saving $15.

Week 2

- Made meal plan for two weeks and did most of grocery shopping, leaving a few produce items to be purchased next week. Stuck to list and found ways to use up extra veggies.

- Made dinner every night this week (except Monday... see next item). Made enough each night to pack both lunches for the next day.

- Used Restaurant.com gift certificate (purchased at 90% off) for a fantastic French meal for my birthday.

Week 3

- Made dinner each night and packed lunches with leftovers. Used up produce before leaving for vacation.

- Didn't purchase a bag of cherries that would have ended up being $8.

- Used ready-to-expire birthday gift certificate for free meal.

- Piggybacked on husband's business trip. Stayed with friends for weekend days and used business stipend for lodging/travel/meals on business days.

- Stalked Southwest Rapid Rewards until a flight opened up on the way there. Continued to stalk and was ecstatic when one opened up for the way back. Canceled originally booked flight to keep in money as Southwest credit, and instead used Rapid Rewards (free) flight.

- Found rental car for $40 for two days including taxes and fees on Travelocity. Husband refrained from upgrading to a convertible even though it was only $25 more. :)

- Packed lunch for the travel day so we wouldn't need to buy stuff on the plane or in the airport.

- Had enough food that we were able to pack lunch to Disneyland. Delicious, healthy, and decidedly cheaper than buying the $8.99 veggie burger.

Week 4

- Again, on the travel note - we chose to use our travel stipend to stay at a B&B with a really outstanding breakfast + free parking instead of a fancy schmancy hotel with no breakfast + paid parking. That way, we could use our daily stipend for other food during the day instead of using it for breakfast. Added bonus = the aforementioned really awesome breakfast.

- Contacted a company about a major customer service faux pas, and was offered $60 in credit. Awesome.

- Had several meals planned for our arrival home so we didn't have to eat out.

- Oh, and went to Disneyland for free (!!) because friend works for Disney.

Impressive, don't you think?

Share To:

Jul 5, 2010

The Burden of Student Loans (Carole)

I ran across this video a few weeks ago on CNN. Go ahead and watch it, and then I'll comment.

I've mentioned before on this blog, that my husband (and I, although the debts were not for my schooling) came out of graduate school with $60,000 in student loans. This was back in 1986. We lived extremely cheaply and only paid for tuition out of our student loans. We were able to earn enough money during the summers and through my job (as a lowly secretary at the university -- so nothing amazing) to pay for our actual living expenses. And, I might add, we never went on food stamps. I'm troubled by this growing trend. But that is another subject for another post.

It is easy to forget while buried in school and taking out student loans, that the day will come when all that money (with interest) has to be paid back. Typically your re-payment begins 6 months after graduation. This date arrives faster than you can imagine. Most loan repayment amounts are several hundred dollars per month, but if you've got debt for graduate school they are often well over $1,000 per month. That is a hefty portion of your brand new salary. Can you really make enough money to live on after your student loan payments?? And most student loans stretch over at least 15 years. That is a long time to be paying back this money.

Repaying student loans is no different than any other debt repayment. Set up a debt snowball and pay it off as fast as possible! But it is best to have a plan before getting into the student loan quagmire. Here are a few ideas to contemplate:

* Go to a local college or university. As a state resident, your tuition is usually about half of what it would be if you are from out-of-state.

* Become a state resident before you attend the school of your choice. A friend of ours who was planning to attend the dental school in Las Vegas moved here a year early, got a job and established residency. He saved himself $15,000/year or $60,000 total.

* Get a bachelor's degree at a college that will not require you to live away from home or pay high tuition. Save student loans for graduate degrees, not a basic college education.

* Apply for any and all scholarships possible. Keep on top of these year to year so you don't lose them. Many students lose these only because they didn't renew them on time.

* Are any grants available for your program? You never have to pay back grant or scholarship money.

* Do everything necessary to be at the top of your class. Top students are often given research or teaching jobs that pay most or all of your tuition.

* Choose your school wisely. Do you really have to have your degree from Harvard?? Think about the debt you will incur (as this fellow in the CNN video didn't). Ask a mature adult who is good with money if this seems like too much money for your educatiaon.

* Determine if your chosen career path is worth the tuition money you will spend. Last fall I heard a caller on the Dave Ramsey Show tell how she and her husband had over $200,000 in student loans for chiropractic school, and now he hadn't been able to find a decent job and they were getting very very frightened for their future. Dave Ramsey informed her that (despite claims from chiropractic schools) these types of doctors do not make the same amount of money typically that an MD does. He felt this couple had way too much debt for the earning potential of a chiropractor. Do your research and make sure it is accurate. Talk to people who are in your field to find out accurate salaries.

*Consider the location of your school. Is it an expensive place to live? Will your school debt be much, much greater because you have to live in New York City or Boston? The mid-west is typically pretty inexpensive as are parts of the south.

I'm certainly not against education in any way! In fact we tell our children that a bachelor's degree is a minimum and that a masters degree (at least) in their field will probably be necessary to compete in today's job market. But don't fool yourself or "blue sky" these kinds of important decisions. Student loans can add a significant financial burden that will follow you for half of your working life if you're not careful.

Like always, plan ahead and live frugally. You'll always be glad you did.

I've mentioned before on this blog, that my husband (and I, although the debts were not for my schooling) came out of graduate school with $60,000 in student loans. This was back in 1986. We lived extremely cheaply and only paid for tuition out of our student loans. We were able to earn enough money during the summers and through my job (as a lowly secretary at the university -- so nothing amazing) to pay for our actual living expenses. And, I might add, we never went on food stamps. I'm troubled by this growing trend. But that is another subject for another post.

It is easy to forget while buried in school and taking out student loans, that the day will come when all that money (with interest) has to be paid back. Typically your re-payment begins 6 months after graduation. This date arrives faster than you can imagine. Most loan repayment amounts are several hundred dollars per month, but if you've got debt for graduate school they are often well over $1,000 per month. That is a hefty portion of your brand new salary. Can you really make enough money to live on after your student loan payments?? And most student loans stretch over at least 15 years. That is a long time to be paying back this money.

Repaying student loans is no different than any other debt repayment. Set up a debt snowball and pay it off as fast as possible! But it is best to have a plan before getting into the student loan quagmire. Here are a few ideas to contemplate:

* Go to a local college or university. As a state resident, your tuition is usually about half of what it would be if you are from out-of-state.

* Become a state resident before you attend the school of your choice. A friend of ours who was planning to attend the dental school in Las Vegas moved here a year early, got a job and established residency. He saved himself $15,000/year or $60,000 total.

* Get a bachelor's degree at a college that will not require you to live away from home or pay high tuition. Save student loans for graduate degrees, not a basic college education.

* Apply for any and all scholarships possible. Keep on top of these year to year so you don't lose them. Many students lose these only because they didn't renew them on time.

* Are any grants available for your program? You never have to pay back grant or scholarship money.

* Do everything necessary to be at the top of your class. Top students are often given research or teaching jobs that pay most or all of your tuition.

* Choose your school wisely. Do you really have to have your degree from Harvard?? Think about the debt you will incur (as this fellow in the CNN video didn't). Ask a mature adult who is good with money if this seems like too much money for your educatiaon.

* Determine if your chosen career path is worth the tuition money you will spend. Last fall I heard a caller on the Dave Ramsey Show tell how she and her husband had over $200,000 in student loans for chiropractic school, and now he hadn't been able to find a decent job and they were getting very very frightened for their future. Dave Ramsey informed her that (despite claims from chiropractic schools) these types of doctors do not make the same amount of money typically that an MD does. He felt this couple had way too much debt for the earning potential of a chiropractor. Do your research and make sure it is accurate. Talk to people who are in your field to find out accurate salaries.

*Consider the location of your school. Is it an expensive place to live? Will your school debt be much, much greater because you have to live in New York City or Boston? The mid-west is typically pretty inexpensive as are parts of the south.

I'm certainly not against education in any way! In fact we tell our children that a bachelor's degree is a minimum and that a masters degree (at least) in their field will probably be necessary to compete in today's job market. But don't fool yourself or "blue sky" these kinds of important decisions. Student loans can add a significant financial burden that will follow you for half of your working life if you're not careful.

Like always, plan ahead and live frugally. You'll always be glad you did.

Share To:

Jul 2, 2010

DIY Gifts: Part 2 (Merrick)

Though I might feel like a good gift giver most of the time, my confidence was definitely shaken when I got married and threw in-laws into the mix.

For my mother-in-law in particular, I spend a lot of time stressing over gifts for her. That's why when I stumbled upon an embellished serving tray on a crafting blog (it's been so long I have no idea what the source is -- sorry), I thought it would make a great gift for her so I immediately saved the link and began my preparations to make the gift.

(pre-grouting)

(pre-grouting)

Materials:

- black serving tray from IKEA - $7

- mini tiles from home depot - $5 (you could also buy a few large tiles and smash them up)

- dry grout - $5 (I only used a tiny bit, so I used this for future projects)

- grout sealer - $5 (same thing -- I only used a tiny bit)

Approximate cost to make this tray: $13

This was a pretty easy project, and when all was said and done it looked awesome. And my mother-in-law really liked it.

Now stop stressing about in-law gifts and go make one of these. It's sure to be a pleaser.

For my mother-in-law in particular, I spend a lot of time stressing over gifts for her. That's why when I stumbled upon an embellished serving tray on a crafting blog (it's been so long I have no idea what the source is -- sorry), I thought it would make a great gift for her so I immediately saved the link and began my preparations to make the gift.

(pre-grouting)

(pre-grouting)Materials:

- black serving tray from IKEA - $7

- mini tiles from home depot - $5 (you could also buy a few large tiles and smash them up)

- dry grout - $5 (I only used a tiny bit, so I used this for future projects)

- grout sealer - $5 (same thing -- I only used a tiny bit)

Approximate cost to make this tray: $13

This was a pretty easy project, and when all was said and done it looked awesome. And my mother-in-law really liked it.

Now stop stressing about in-law gifts and go make one of these. It's sure to be a pleaser.

Share To:

Jul 1, 2010

Baby Announcements (Janssen)

I am not the crafty type. At all.

But, long before we were expecting our first baby, I knew my husband really wanted us to send out announcements after our child was born.

I also knew that if we were going to send them out I wanted them to be 1) inexpensive and 2) good looking.

If you've ever looked at baby announcements online, you know that you can spend an absolute fortune on them. We had no fortune, absolute or otherwise, so this wasn't really a good option for us.

Instead, I figured out what components I needed and how little I could spend on each part:

But, long before we were expecting our first baby, I knew my husband really wanted us to send out announcements after our child was born.

I also knew that if we were going to send them out I wanted them to be 1) inexpensive and 2) good looking.

If you've ever looked at baby announcements online, you know that you can spend an absolute fortune on them. We had no fortune, absolute or otherwise, so this wasn't really a good option for us.

Instead, I figured out what components I needed and how little I could spend on each part:

- I needed a photograph. We have a nice camera, so we could have taken it ourselves, but happily, a friend of ours is professional photographer and she offered to come take some newborn pictures for free. That's my favorite price. If you don't have a nice camera, I bet you know someone who does and might let you use it for a few hours - it seems like everyone I know owns an SLR now.

- I needed an announcement design. I spent quite a lot of time (and forced my husband to also) browsing the announcements on Minted so I could get some ideas and see what kind of things we both liked. Then we mocked up a few of our own in Photoshop. Also free!

- We need to actually print the announcements. I made our mockups to be a 4x6 (standard picture size) and then plan to upload them to Snapfish (Shutterfly and other online photography places also would work). When you sign up for an account, you get some number of free prints (depends on what current deal is going on - sometimes it's 20, sometimes it is 50) and you can usually print them right to your local drugstore or Walmart. Freeeeeee (depending on how many you need, of course).

- Envelopes. I hoarded all my Staples rewards dollars and waited until invitation envelopes (which fit a 4x6 perfectly) went on sale and then I bought those. Free again!

- Stamps. Sadly, I haven't yet figured out a great way to get discount postage, although I know it is possible. But when stamps are the only thing you're paying for, I figure that's pretty good.

Share To: