I am willing to live frugally now so that in the future I can be financially independent.

I was listening to Dave Ramsey's podcast recently and a woman in her late forties called in to say that she was really anxious to start paying down their debts and getting ahead financially. Her husband (who was in his early fifties), however, was not at all on-board, feeling that they were just fine the way they were. After all, they made a pretty substantial income and they could certainly afford their monthly payments. Dave Ramsey asked her how much cash they would have if they sold everything they had, including cars and their house, and paid off all their debts. Her answer? About $50,000.

Can you imagine being ten years from retirement age and having a net worth of only $50,000? This woman's husband had probably been working for 30 years, which means he had less than $2,000 per year to show for all his hard work. You could not live for very long on $50,000, especially when that $50,000 is tied up in your house and car.

This couple is in the financial position of people a fraction of their age - people in their late twenties, perhaps. How will this couple, or others who live like them, ever be able to retire? If you spend everything you earn, you are just treading water, never getting closer to being able to retire and to letting your money earn enough to cover your expenses.

At some point, wouldn't it be nice to wake up every morning and go to work just because you WANT to, and not because you NEED to in order to keep a roof over your head?

Ideally, after thirty years of work, you'd have a house that you owned free and clear, one or two cars that were completely paid off, an emergency fund that could cover your living expenses for 6-12 months, and some hefty retirement and investment accounts. And it'd be even more awesome if, because you'd been frugal, you'd also been able to be generous with your money, and to have taken some nice vacations as a family or a couple over the years.

Most of us will make more money as time goes on - better jobs, more experience, more responsibility, new raises, etc - but if spending increases at the same rate (or, terrifyingly, even faster), we'll never be able to retire because our expenses will be increasing and we'll never move any closer to the goal of being able to live without jobs to support us.

If you pay for a big house, fancy cars, a boat or ATVs, ritzy vacations or whatever your splurge of choice is, but you pay for it all on credit and you'd lose it if the economy tanks (does that sound familiar?) or if you lost your job, you. are. not. wealthy. You're just living like you are. Wealth is owning your own possessions, being prepared for emergencies, and not being dependent on your next paycheck in order to keep your BMW sitting in the driveway.

My goal is for each year to bring us closer to financial independence - for our lifestyle to not be dependent on a steady paycheck. Instead, ideally, our savings and investments will grow enough to cover all our bills and still continue to grow. I'm willing to watch my spending and practice frugality now in order to see progress on a monthly and yearly basis toward my long-term goals, so that when my husband and I are in our fifties, we aren't in the same financial situation we are in today.

Feb 26, 2010

Feb 25, 2010

Save Money By Cooking like the Kennedys! (Carole)

Years ago I read, that Rose Kennedy (mother of JFK, RFK and recently deceased Teddy) served the same seven meals every week. Since the Kennedy clan has been in the multi-multi-millionaire category since the 1930’s, I’m confident that Rose was not actually in the kitchen with an apron on, whipping up these nightly meals. But, however these meals were prepared, the message is that she had a limited list of dinner main dishes that kept life simple.

Like your family, mine would probably revolt if I only served 7 meals – over and over and over again. So I’ve increased mine to 37. There’s nothing magical about that number, it’s just what I came up with about 10 years ago. I sat down one day and listed all the decently easy-to-make main dishes my family liked. I can hardly express how much this little list has helped me over the years.

I am not an amazing cook, nor do I love to cook. However, since it is so much cheaper and healthier to eat at home than it is to eat out, I have cooked most of the meals in our house for the past 26+ years. And I have found it is much easier to deal with dinner time if I am extremely familiar with the main dish recipe I’m cooking -- I've also found that my family eats more of the meal if I serve a dish they recognize.

My list of 37 main dishes are all family favorites. About once a year I update it – whacking out anything I’m tired of making (or have ceased to be favorites) and adding in the occasional new recipe that I’ve tried and everyone found tasty. So, it is a list that continues to evolve.

I keep this list as a Word document on my computer (for easy updating) and print it out. I then tape the list to the inside of one of my kitchen cupboards for easy reference. It is titled “Main Dishes that David Likes.” Since he and I have very different palates, I also use this list as a reminder of what he will enjoy eating (mild and creamy) – versus what I might enjoy (hot and spicy). I’ve highlighted the REALLY EASY meals on the list, so that in a time or ingredient pinch, I can remember what makes a good meal without taking either too much time or having to run to the grocery store for a special ingredient. I also have all the crock pot recipes grouped together.

Having a list like this saves me a huge amount of time and effort when planning my weekly menu – no more digging through piles of cookbooks, recipe cards or websites for ideas of what to serve. Some of these 37 recipes don’t get made more than a couple of times a year (Manicotti). While other recipes are made every couple of weeks (Quiche). It just depends on what sounds good to me at the time.

This simple list also helps me when I’m at the grocery store or looking through the store’s weekly sale flier. Because my menu is pretty standard month to month, I know what ingredients I traditionally need, so when I see them on sale I can stock up (saving lots of money). It also keeps me from having to buy some odd ingredient and then having it sit in the back of the fridge until I throw it away (wasting lots of money).

I’ll share my list with you and maybe it will get you thinking of your own family favorites. Feel like sharing your favorite go-to meal ideas?? We'd love to hear them!!

- Chicken Bacon Wrap - crock pot

- Pot Roast - crock pot

- Beef Stroganoff - crock pot

- Chicken a la King - crock pot

- Stew - crock pot

- Beef Dip Sandwiches - crock pot

- BBQ Spareribs - crock pot

- Taco soup - crock pot

- Quiche

- Pork Loin Roast

- Pepperoni Alfredo

- Salmon

- Tuna over Rice

- Mini Pizza

- Ham and Baked Corn

- Breakfast for dinner (waffles, pancakes, eggs and toast)

- Tacos

- Hamburgers

- Baked Chicken

- Fried Chicken

- Baked Pork Chops

- Chicken Packets

- Potato Soup

- Tuna and Pasta casserole

- Italian Pastry Bake

- Shepard’s Pie

- Manicotti

- Chili and Corn Bread

- Enchiladas

- Chicken Pot Pie

- Crepes and Fruit Smoothies

- Stuffed Baked Potatoes

- Grandma Henrie’s Meatballs over rice

- Peanut Butter Chicken Soup

- Chicken Salad

- Ranch Chicken

- Chicken Divan

Share To:

Feb 24, 2010

Unnecessary Expenses: Part 1 (Merrick)

During a vacation to visit my parents a few weeks ago, my mom and I got talking about frugal living – this blog has taken over our brains and allowed us to think of nothing else! As we discussed this topic, she mentioned hearing on the news a story about a young woman who had recently been offered a job at Las Vegas’ new City Center, and how this job had been a godsend since “she just didn’t know where the money for next month’s cable bill was going to come from." *

Do we, as spoiled people of the twenty-first century, have this same mentality? Are we stressing and stretching our financial limits in order to have luxuries that we’ve been brainwashed to think are necessities?

I think we’re all guilty of this at one time or another, thinking that we just can't live with out [insert item here], even though we don't really need it or can’t afford it. This mentality results in credit card debt, living above our means, and having no savings or emergency funds.

Over the next few posts I’ll be talking about some of these unnecessary expenses, how you can overcome the “I need it now!” mentality, and how (in many cases), there are much cheaper options that are just as good.

*not an exact quotation

Do we, as spoiled people of the twenty-first century, have this same mentality? Are we stressing and stretching our financial limits in order to have luxuries that we’ve been brainwashed to think are necessities?

I think we’re all guilty of this at one time or another, thinking that we just can't live with out [insert item here], even though we don't really need it or can’t afford it. This mentality results in credit card debt, living above our means, and having no savings or emergency funds.

Over the next few posts I’ll be talking about some of these unnecessary expenses, how you can overcome the “I need it now!” mentality, and how (in many cases), there are much cheaper options that are just as good.

*not an exact quotation

Share To:

Feb 23, 2010

Why Live Frugally Now? Reason #3 (Janssen)

I am willing to live frugally now so that my money can become an additional income earner. I think this one reason is the single most important way that your frugality can really pay off in a tangible and very major way.

If I spend every dime I make, the only money coming into my household is the money that comes via my paycheck. If, instead, I can resist spending $50 or $100 or whatever amount of money per month and put that money in a Roth IRA or in mutual funds, that money now becomes an additional income earner. (As my dad likes to joke, "I say to my money 'Get off the couch and go get a job!'"). That money can earn interest, day in and day out, while you exert no additional effort. Who doesn't like the idea of your money working for you?

And, of course, the earlier you can get your finances under control enough to have money to invest, the longer that money will work for you. Who wouldn't rather have your dollars working hard for 10 years instead of 5 or 30 years instead of 20?

I'm willing to guess most of us hate interest when it's us paying it (22% for a burger you paid for on your credit card, anyone?), but when interest is working in my favor, well, I love the fact that it doesn't take weekends or holidays off and that it never gets sick or needs a personal day.

If you can discipline yourself enough to live frugally today, you can reap the rewards of it for the rest of your life and in a really substantial way (we're talking hundreds of thousands, if not millions of dollars, that you did not have to earn yourself because your money, which you already earned, is now working for you).

It's worth asking yourself how much suffering $25 or $50 or $100 out of your monthly budget would cause you. Would it be worth it?

If I spend every dime I make, the only money coming into my household is the money that comes via my paycheck. If, instead, I can resist spending $50 or $100 or whatever amount of money per month and put that money in a Roth IRA or in mutual funds, that money now becomes an additional income earner. (As my dad likes to joke, "I say to my money 'Get off the couch and go get a job!'"). That money can earn interest, day in and day out, while you exert no additional effort. Who doesn't like the idea of your money working for you?

And, of course, the earlier you can get your finances under control enough to have money to invest, the longer that money will work for you. Who wouldn't rather have your dollars working hard for 10 years instead of 5 or 30 years instead of 20?

I'm willing to guess most of us hate interest when it's us paying it (22% for a burger you paid for on your credit card, anyone?), but when interest is working in my favor, well, I love the fact that it doesn't take weekends or holidays off and that it never gets sick or needs a personal day.

If you can discipline yourself enough to live frugally today, you can reap the rewards of it for the rest of your life and in a really substantial way (we're talking hundreds of thousands, if not millions of dollars, that you did not have to earn yourself because your money, which you already earned, is now working for you).

It's worth asking yourself how much suffering $25 or $50 or $100 out of your monthly budget would cause you. Would it be worth it?

Share To:

Feb 22, 2010

Extra! Extra!

It appears that our blog has swept the nation so rapidly during its almost two months of existence that we made the New York Times front page!

If you mail us your copy of the New York Times, we would be MORE than happy to send it back with an autograph :)

If you mail us your copy of the New York Times, we would be MORE than happy to send it back with an autograph :)

Share To:

Feb 19, 2010

Save Big Money When Buying a House - Part 2 (Carole)

Once you have your personal mortgage payment (24% or your monthly take-home pay) number in hand, it is time to go looking for a house. Here are a few ways to buy a house for less:

- Buy a foreclosure. In today’s sad housing market there are some amazing deals to be made on beautiful homes that are being foreclosed on. Foreclosures happen every day in every state. However, right now, there are thousands (if not millions) of homes in foreclosure (take a peek at HUD homes too -- they are merely foreclosed homes that had an FHA loan). The previous owner could no longer afford the monthly payment and the bank has had to take ownership of the house back. In a foreclosure you buy the house from the bank. The bank does not want to own the house and they are often willing to sell it at a substantial discount in order to get it back into a mortgage where they can make money off the interest again.

- Buy a Short Sale. A short sale is similar to a foreclosure, except that the owner still technically owns the house but is behind on their payments and will soon go into foreclosure unless they sell it. The delinquent owner is trying to convince the bank to let them sell the house to a new owner for less than they paid for it and have the bank eat the difference between the old loan and the new loan – rather than the owner still owing that money to the bank (BEWARE: the seller will be taxed on the "forgiven" part of their home loan -- that can be extremely expensive. Doing a short sale also goes on your credit report). It is a horrible thing to be a seller in this category, but the new owner gets a great deal – sometimes saving 50% on the house.

- Buy a modest home in a great neighborhood. Remember the old real estate saying: Location, Location, Location. This is ALWAYS TRUE. The value of your house is always going to be tied very tightly to where your house sits. If you have a modest home, but it sits in a beautifully cared for, desirable neighborhood, it will be worth more than if you have a gorgeous home in a declining neighborhood or next to a gas station or freeway. Be very aware of what surrounds the house you buy. Good neighborhoods tend to see their home values increase over time and your demure home will climb right along with it – at a much faster and higher rate then a great home in a medium or declining neighborhood.

- Buy a fixer-upper. If you buy that modest home in a good neighborhood AND it needs some work – you are getting a home run. (As long as the work to be done is not too extensive.) I’ve known many, many people who have moved into a house that had a nice location, but it needed some new paint colors, some lawn care and maybe a few new roof tiles. The price for a house with these kinds of problems goes WAY down – often tens of thousands of dollars. Old kitchens and bathrooms especially drive a house price down like nothing else -- remember this tip when you're selling yours. If you’re willing to put in a bit of elbow grease, you can really get a nice home at a cheap price and turn it into your dream house.

- Stay put: Another way to save big money on a house is to stay put. Buy a house that meets your needs and live in it for 50 years. The house will appreciate around you. Even in a less than desirable neighborhood. Buy something modest and make it work. Those children who need so much space when they’re teens, move out sooner than you’d guess. Before you know it you’ve got an empty nest. Might as well let them share bedrooms and bathrooms for a few years (it builds character!) and not end up with the mega-house to heat and clean after they’ve all move out. Inflation will work in your favor as long as you are not constantly restarting your 15 or 30 year mortgage by moving. One of our older relatives bought a home back in the 1930’s for about $12,000. His daughters sold it when he passed away in the 1990’s for over $400,000. Real estate – over enough time – does go up.

- Have a long-term plan: I have a good friend who has owned 4 homes in the nearly 20 years I’ve known her. They have lived the last 8 years in a FABULOUS home in one of the very exclusive guard-gated neighborhoods in our area. From what I hear, their house is paid for. But they had a plan – all those years ago on how to get there. House One: When their oldest child was very small, they purchased a HUD home. Take a look at the last link for the rules on buying a HUD home. It was a small home in a medium-level neighborhood. But they paid pennies on the dollar of what it was worth. They redid some tile, painted it inside and out and fixed up the yard and sold it 3 years later for tens of thousands of dollars more than they bought it for. House Two: They found a builders close-out house in a brand new neighborhood that was being sold $25,000 below the cost of other similar homes, because it was the last one of its kind and the builder just needed to sell it. They put in a nice yard, and kept it in good shape and 3 years later they sold it for tens of thousands of dollars more than they paid for it. Are you seeing a pattern?? House Three: They built house #3 and the husband acted as general contractor (saving tens of thousands of dollars). He used every connection he had among builders, carpet sellers and such to keep his cost very low. This house was in a guard-gated community near the airport. So, even though it was in an upscale neighborhood, the noisy location kept the lot prices low. This was a beautiful home with many designer amenities, but all installed following a strict budget. They lived in this house for about 5 years – and you guessed it, made a killing when they sold it. House Four (current home): Again they built this home and acted as their own contractors. This house is massive and spectacular. And paid for. All because they had a plan and were willing to put in some work to get there.

Share To:

Feb 18, 2010

Unexpected Expenses: Gifts - Part 3 (Merrick)

As far as gifts go, wedding gifts are always a budget killer, in my opinion. You can probably get away with cheaper gifts at baby showers since it’s hard to tell the difference between a $5 outfit and a $50 outfit; but wedding gifts are slightly less easy to disguise, especially when you get items the couple has registered for, so they know exactly how much you spent and how cheap you are.

Therefore, to avoid this problem, I’ve come up with a standard, inexpensive, but heartfelt, wedding gift that I give to anyone and everyone getting married: A Cookbook.

Now, this is not just any cookbook. I actually got the idea from my sister, Janssen, who put together a cookbook for our wedding of all her favorite recipes. For one, this was an extremely thoughtful gift since she not only took the time to compile all the recipes, she also put little blurbs at the beginning of each recipe telling where she found it, what she serves it with, why she likes, it, etc. Second, it was the perfect gift because the moment I was married and presented with my first week of cooking for two people, I suddenly couldn’t remember one single thing my mom had ever cooked. What did we eat for the last 20 years of my life?!

When the wedding announcements began pouring in, I thought back to this perfect gift and decided to use it as my standard, cheap, thoughtful wedding gift.

I drew up a cute design for the front, compiled all my favorite recipes (I’m constantly adding to this), wrote funny blurbs for each recipe, and then saved it all on my computer. Every time we get invited to a wedding, I print out the cookbook, put it in a $3 binder, wrap it in dollar store wrapping paper, and voila! The cheapest wedding gift you’ll ever give, and yet it’s the one I get requests for from friends who have upcoming weddings.

Bottom line is this: wedding gifts can be expensive, and sometimes we feel obligated to buy something that goes beyond our budget so you don’t feel like a cheapskate. But if you can come up with a gift that is thought out and meaningful, but also inexpensive, you get the best of both worlds.

So, does this get your creative wheels turning? I’d love to hear your ideas for inexpensive wedding gifts.

Therefore, to avoid this problem, I’ve come up with a standard, inexpensive, but heartfelt, wedding gift that I give to anyone and everyone getting married: A Cookbook.

Now, this is not just any cookbook. I actually got the idea from my sister, Janssen, who put together a cookbook for our wedding of all her favorite recipes. For one, this was an extremely thoughtful gift since she not only took the time to compile all the recipes, she also put little blurbs at the beginning of each recipe telling where she found it, what she serves it with, why she likes, it, etc. Second, it was the perfect gift because the moment I was married and presented with my first week of cooking for two people, I suddenly couldn’t remember one single thing my mom had ever cooked. What did we eat for the last 20 years of my life?!

When the wedding announcements began pouring in, I thought back to this perfect gift and decided to use it as my standard, cheap, thoughtful wedding gift.

I drew up a cute design for the front, compiled all my favorite recipes (I’m constantly adding to this), wrote funny blurbs for each recipe, and then saved it all on my computer. Every time we get invited to a wedding, I print out the cookbook, put it in a $3 binder, wrap it in dollar store wrapping paper, and voila! The cheapest wedding gift you’ll ever give, and yet it’s the one I get requests for from friends who have upcoming weddings.

Bottom line is this: wedding gifts can be expensive, and sometimes we feel obligated to buy something that goes beyond our budget so you don’t feel like a cheapskate. But if you can come up with a gift that is thought out and meaningful, but also inexpensive, you get the best of both worlds.

So, does this get your creative wheels turning? I’d love to hear your ideas for inexpensive wedding gifts.

Share To:

Feb 17, 2010

Why Live Frugally Now? Reason #2 (Janssen)

The second reason I think it is worth it to live frugally now is so I can stay out of debt.

Debt is a pervasive part of our society's way of living, but I am determined to avoid it. After all, if you take on debt to pay for an item, you have to pay interest for it. Since I can hardly stomach the idea of paying full price for an item, you can imagine how much I like paying full price AND interest on an item (hint: not even a little bit).

Having debt also means you are obligated to pay an additional monthly bill, which means less of your income is going to you and more of your income is going to pay for something that you bought months or years ago! You're paying for a meal that's long since been eaten or for a shirt that isn't new and thrilling anymore (and might already be stained or snagged or shrunk). Your expenses are going up instead of down and the money you could have spent on something else, something more worthwhile and longlasting, is now tied up in a monthly payment.

As several people mentioned in the comments here, it is very easy to get into debt (how many credit card offers do you get in the mail every month?), and very difficult to get out of. Swiping that card for a fun vacation or taking a line of store credit to pay for a new couch takes very little effort, but you'll end up paying far more than the ticket price of those items, and you'll be forced to pay on them for years afterwards.

And if you are living on the very edge of your means, instead of with some degree of frugality, debt may be your only option when your water heater explodes or when you have to pay for funeral expenses unexpectedly. And then you're paying interest for the most unpleasant things you can imagine, as if paying for them the first time wasn't bad enough.

I am more than willing to live frugally so that I don't pay extra money for items, vacations, or furniture, so that my income isn't all obligated to a credit card company (I want my income to be my money, not Visa's or Mastercard's or American Express'), and so that I don't have to spend huge amounts of effort trying to get back out from under that debt and own my own money again.

Debt is a pervasive part of our society's way of living, but I am determined to avoid it. After all, if you take on debt to pay for an item, you have to pay interest for it. Since I can hardly stomach the idea of paying full price for an item, you can imagine how much I like paying full price AND interest on an item (hint: not even a little bit).

Having debt also means you are obligated to pay an additional monthly bill, which means less of your income is going to you and more of your income is going to pay for something that you bought months or years ago! You're paying for a meal that's long since been eaten or for a shirt that isn't new and thrilling anymore (and might already be stained or snagged or shrunk). Your expenses are going up instead of down and the money you could have spent on something else, something more worthwhile and longlasting, is now tied up in a monthly payment.

As several people mentioned in the comments here, it is very easy to get into debt (how many credit card offers do you get in the mail every month?), and very difficult to get out of. Swiping that card for a fun vacation or taking a line of store credit to pay for a new couch takes very little effort, but you'll end up paying far more than the ticket price of those items, and you'll be forced to pay on them for years afterwards.

And if you are living on the very edge of your means, instead of with some degree of frugality, debt may be your only option when your water heater explodes or when you have to pay for funeral expenses unexpectedly. And then you're paying interest for the most unpleasant things you can imagine, as if paying for them the first time wasn't bad enough.

I am more than willing to live frugally so that I don't pay extra money for items, vacations, or furniture, so that my income isn't all obligated to a credit card company (I want my income to be my money, not Visa's or Mastercard's or American Express'), and so that I don't have to spend huge amounts of effort trying to get back out from under that debt and own my own money again.

Share To:

Feb 16, 2010

Save Big Money When Buying a House - Part 1 (Carole)

Your house is probably the most expensive single item you will ever buy. Because of that, it only makes sense that it can also give you a tremendous opportunity to save a ton of money when you buy it. If you save 50% on a $20 blouse you only save $10. If you save 50% on a $200,000 house, you save $100,000! That is some serious saved cash. Conversely, being reckless or uninformed when buying a house can cost you the same kind of money.

Here is an important, basic piece of information that can help you save money when buying a house:

The 24% Rule:

Your monthly mortgage should be no more than 24% of your monthly take-home pay. That means if you bring home $2,000/month then your monthly mortgage payment should not be more than $480. If you bring home $5,000/month then your monthly mortgage payment should not be more than $1,200. Take the time to figure out your own monthly take-home paycheck amount, and then multiply that dollar number by .24 to determine your upper limit for a monthly mortgage payment.

Here is a simple mortgage calculator that will help you easily figure out the total amount you should spend on a house and still keep your mortgage payment within your money limit.

What if you already own a house? Do the calculations anyway, and see where your mortgage payment falls compared with 24% of your monthly take-home pay. Do you own a house that you can truly afford or is it too expensive?

It’s good to know this information.

Interestingly, when David and I purchased our first home back in 1989, the rule-of-thumb on house payment percentage was 18%. That is substantially different from today’s conventional wisdom of 24%. I would guess there were a lot fewer foreclosures and short sales back in the 1980’s with that 18% number. If you’ve ever been a homeowner, you know that your mortgage payment is not the total cost of home ownership. In addition, there are:

1. Property Taxes

2. Homeowners Insurance

3. Home Repairs

Just these three expenses add up to thousands more $$ every year. Owning a house is certainly a worthwhile goal, but it is also expensive. Be wise.

I have only been a casual observer of homebuyers over the past couple of decades, but I think this raise in percentage from 18% to 24% has less to do with the rising cost of housing than with people’s desire to buy something bigger and fancier than in years past, and the personal motivation of most realtors and bankers to convince you that you should. Our first realtor (back in 1989) told us that we could afford to buy ANY house in the town we lived in! Wow, those were heady words -- I still remember them 21 years later!! Who knows, maybe we could have. But with three small children, student loans and a large business loan, we knew this would be a huge financial mistake! We stuck to the 18% rule and bought something nice, but normal. Many realtors will tell you anything. However, after they earn their hefty commission, you are on your own to pay that huge monthly payment.

Amazingly, many of those who are currently facing foreclosure or a short sale bought homes that were priced FAR ABOVE the reasonable 24% rule. Some folks purchased homes that require a monthly mortgage payment of nearly 50% of their take-home pay! That is simply too much to be paying for a roof over your head. Illness, reduced salary, job loss or an adjustable rate mortgage can push you into financial ruin very quickly with a house payment in this range.

You just might want to consider using the smaller 18% number when purchasing your next home. This will go a long way toward keeping your financial future secure. Remember, the lower you can keep your monthly bills, the more money you can set aside to cover those inevitable rainy days and still carefully invest for your FABULOUS future.

In my next post I will share simple ideas for saving big $ when buying a house.

Share To:

Feb 15, 2010

Unexpected Expenses: Gifts - Part 2 (Merrick)

A piece of mail that frequents my mailbox is baby shower invitations. While there are lots of great gifts out there at the stores for baby showers, this is a great chance to save some money, and get creative.

Today I’ll share one cheap, fun, and creative idea for a baby shower gift that also requires very little skill.

I made these onesies for a recent baby shower. As we all know, baby clothes are a favorite shower gift – everyone always “oohs” and “ahhs” over the cute outfits the mom-to-be receives. Well if it’s a hand made outfit like the one pictured above, it’s sure to impress. The best part about this is that I spent less than five dollars for this baby gift.

The onesies are from Kmart and were roughly $8.00 for a pack of five. That’s $1.60 each, so since I made two, that’s $3.20 for the onesies. Then I bought the fabric from Joann’s at about $1.99/yd, and since I needed so little, I got a quarter of a yard of each fabric. That’s about $0.50 per color, totaling $1.00 for the two fabrics. I had matching thread, but it would also be very cute to have a contrasting color of thread, and that saves you a few pennies if you already have thread lying around at home.

Once all the materials were assembled, I cut out the fabric in my desired shape (elephant and dinosaur), and then zigzag stitched them to the onesie with my sewing machine (you could just as easily hand stitch these)

Such a simple gift, but fun, cheap, and heartfelt.

There are so many other good ideas out there that are just waiting to be copied. Etsy has plenty of great ideas, like this cute one for a boy baby shower. Or you can find inspiration from one of my good blog friends.

Gifts do not have to be a burden or a budget buster. With a little time and creativity, you can create inexpensive, fun, and generic baby shower gifts that will leave everyone impressed – your budget included.

Today I’ll share one cheap, fun, and creative idea for a baby shower gift that also requires very little skill.

I made these onesies for a recent baby shower. As we all know, baby clothes are a favorite shower gift – everyone always “oohs” and “ahhs” over the cute outfits the mom-to-be receives. Well if it’s a hand made outfit like the one pictured above, it’s sure to impress. The best part about this is that I spent less than five dollars for this baby gift.

The onesies are from Kmart and were roughly $8.00 for a pack of five. That’s $1.60 each, so since I made two, that’s $3.20 for the onesies. Then I bought the fabric from Joann’s at about $1.99/yd, and since I needed so little, I got a quarter of a yard of each fabric. That’s about $0.50 per color, totaling $1.00 for the two fabrics. I had matching thread, but it would also be very cute to have a contrasting color of thread, and that saves you a few pennies if you already have thread lying around at home.

Once all the materials were assembled, I cut out the fabric in my desired shape (elephant and dinosaur), and then zigzag stitched them to the onesie with my sewing machine (you could just as easily hand stitch these)

Such a simple gift, but fun, cheap, and heartfelt.

There are so many other good ideas out there that are just waiting to be copied. Etsy has plenty of great ideas, like this cute one for a boy baby shower. Or you can find inspiration from one of my good blog friends.

Gifts do not have to be a burden or a budget buster. With a little time and creativity, you can create inexpensive, fun, and generic baby shower gifts that will leave everyone impressed – your budget included.

Share To:

Feb 11, 2010

Why Live Frugally Now? Reason #1 (Janssen)

I worry about money. I imagine there are some people who absolutely do not worry about money at all, ever, no matter how little they're making or how deeply in debt they are, but I cannot imagine such a life. I need my financial life to be in order or I spend a lot of time worrying about it and feeling uneasy.

For me, the #1 reason to live frugally now is the peace of mind it brings.

If you are not saving any money, if you're living on virtually every cent of your income, you are only one unexpected expense away from disaster. If your car suddenly dies or a child gets sick or you/your spouse gets laid off or your employer gives out pay cuts, or you suddenly owe taxes when you expected a tax return or your roof starts leaking, and you don't have money tucked away, you're in trouble.

If any of those things (or the millions of other things that can go wrong) happen and you have no way at all to pay for them, you're left to suffer the consequences.

When our house's air conditioner had to be completely replaced last summer (to the tune of several thousand dollars), it was unpleasant, of course; I could think of a hundred things I would have rather spent that money on (every last one of them more fun than an air conditioner). But, thankfully, it didn't break the bank for us. We had savings to pay for it in cash and not think about it again. We didn't have to sell our car. We didn't have to put it on our credit card at 100000% interest. We didn't have to live on ramen noodles for six months. We didn't have to ask either of our parents to loan us money. It was inconvenient, but it was not a tragedy, and it didn't put us in a tight situation.

Living within your means, enough that you can have an emergency fund, is the only thing that acts as a buffer between you and unexpected, unwanted financial tragedy. If you do not have savings or an emergency fund to pull you through those events, you'll have to take on debt to cover the expense.

And avoiding debt is the second biggest reason I am willing to live frugally now. Stay tuned!

For me, the #1 reason to live frugally now is the peace of mind it brings.

If you are not saving any money, if you're living on virtually every cent of your income, you are only one unexpected expense away from disaster. If your car suddenly dies or a child gets sick or you/your spouse gets laid off or your employer gives out pay cuts, or you suddenly owe taxes when you expected a tax return or your roof starts leaking, and you don't have money tucked away, you're in trouble.

If any of those things (or the millions of other things that can go wrong) happen and you have no way at all to pay for them, you're left to suffer the consequences.

When our house's air conditioner had to be completely replaced last summer (to the tune of several thousand dollars), it was unpleasant, of course; I could think of a hundred things I would have rather spent that money on (every last one of them more fun than an air conditioner). But, thankfully, it didn't break the bank for us. We had savings to pay for it in cash and not think about it again. We didn't have to sell our car. We didn't have to put it on our credit card at 100000% interest. We didn't have to live on ramen noodles for six months. We didn't have to ask either of our parents to loan us money. It was inconvenient, but it was not a tragedy, and it didn't put us in a tight situation.

Living within your means, enough that you can have an emergency fund, is the only thing that acts as a buffer between you and unexpected, unwanted financial tragedy. If you do not have savings or an emergency fund to pull you through those events, you'll have to take on debt to cover the expense.

And avoiding debt is the second biggest reason I am willing to live frugally now. Stay tuned!

Share To:

Feb 10, 2010

Save Big Money on Rent (Carole)

You will remember, that I am endorsing the idea of living WAY below your take-home pay. When you’re young and your income is probably at its lowest point for your earning life, that probably seems nearly impossible. However, there are ways. . .

The first one I want to mention has to do with reducing (or even eliminating) your housing costs. “How can this be??” you ask. Let me share some time-tested ideas.

When my husband was in graduate school we lived exclusively on my piddly secretary income. We were determined to only use student loans for tuition. My annual salary was about 1/3 of what we now make every month. Ha! Of course, money was worth a bit more back then and life in the mid-west is always cheaper than in the west. But still. We were living on extremely limited funds. To say the least.

That meant no money for rent.

So, we had to figure out some other way. Let me interrupt myself here to say what a blessing it was that my father-in-law insisted that David and I put together a budget for our 4 years of graduate school before we got married. He wanted to make sure that we had a plan for how we were going to survive until we were done. This exercise was when we realized we couldn’t afford a roof over our heads. At least not a very nice one in a safe area of town. So, like I said before, we got creative, and this is what we did:

- House sat for an elderly woman who was serving a religious mission for one year. She didn’t really need rent money, and was mostly wanting a clean, responsible couple to watch her house and keep the heat on while she was away. We paid her $50 per month – that was really cheap even back in the early 1980’s. Since her house was fully furnished, we also didn’t have to buy any furniture.

- House sat for a couple that took an extended vacation. They actually paid us to keep their house looking lived-in while they were away. I think we fed their cats too. This was a beautiful home and she was an incredible housekeeper. I learned a lot from living in her home. I still fold my towels like she did.

- House sat for a couple who were selling a 2nd home. This 2nd home was the MOST DARLING little bungalow. It was cozy and cute in a nice neighborhood. This was our first non-furnished place, so we finally had to break down and get some furniture --used, of course. It was fun to finally have a few things of our own. The house sold because a potential buyer loved that I was baking bread and knitting when she came over. We lived there rent-free for several months.

- House sat for a woman who was beginning to shows signs of senility. She was sweet and lovely, but extremely forgetful. Her two grown children wanted someone in the house to make sure she ate her meals and could call for help if something went wrong. She lived in a very upscale neighborhood right on Lake Michigan, and we lived in her lovely attic for free for about a year and a half. Right through graduation!

- We had other friends who were grounds keepers on a medium sized estate just on the edge of town. They lived in a darling little carriage house with only minimal duties of mowing the grass and watching over the property while the owners were frequently out of town. They not only lived rent-free, but made a decent little salary. All while the husband was in school.

- Another friend of ours was a single fellow who lived with a very elderly gentleman who needed someone around to help him with daily tasks and just wanted some company in the evenings. This friend not only lived rent-free, he also had free groceries. He had this job through 4 years of dental school. And amazingly when the sweet man passed away a few years later, he left his beautiful house to our friend. Tom still lives there with his own family.

After school was done, we still didn’t have any money. And we had a baby. We moved to a small town in the middle of nowhere for David’s first job and amazingly found more opportunities to house sit. Because we had learned that word-of-mouth is the best way to find rent-free opportunities, we started asking around. Within a week a businessman in this small town called us up (sight unseen) and wanted us to live in a house he had been trying to sell for over a year. It was a large ranch-style home on a beautiful street. We stayed about 4 months until the house sold. Word spread that we would make a house look nice and smell nice, and we got a 2nd house-selling gig right away. That house never sold, but I don’t feel responsible for that failure J -- it had a bad location. We lived there for many months.

By now we had our 2nd baby on the way and it became difficult to convince people how clean and attentive we could be with TWO children running around their house. But we weren't ready to pay rent yet, so we turned to the time-tested apartment manager job. This opportunity came through the newspaper. We managed a small complex with about 20 units. This was certainly a lot of work, but I learned a lot and we enjoyed the free rent for another 10 months. Finally, we moved to a larger city for a new job and managed a complex of 100+ townhouses for about 4 months. I found that VERY hard to handle with 2 tiny children. But by now we felt we could afford rent and found a nice duplex (where we negotiated the rent price down a few hundred dollars per month – we’d learned as apartment managers that all rent is negotiable) and lived there until we finally bought a house.

The bottom line here is that we lived in BEAUTIFUL places that we could never have afforded -- for nothing. We saved thousands and thousands of dollars over an almost 5 year period of time just because we thought outside the box and asked around. You just never know. . . Living frugally is a lot more exciting than you'd guess.

Share To:

Feb 9, 2010

Unexpected Expenses: Gifts - Part 1 (Merrick)

As we’ve talked about budgeting on this blog, “unexpected expenses” have been mentioned a few times – those necessary expenses that pop up during the month and throw off your meticulous budgeting. Mandatory car repairs, or unexpectedly high gas bills can be among these unexpected expenses, but what about gifts? Just about every month there is a wedding, a baby shower, or a birthday that pops up – you run out at the last minute to buy a gift and end up blowing your budget. Can you relate to this situation?

Philip and I are a young married couple, freshly out of college, with tons of friends getting married and popping out babies right and left. On top of our own monthly expenses, we can’t really afford to fork out thirty or forty bucks for a nice gift every time we get a wedding, baby shower, or birthday party invitation. But we also don’t want to be that couple that doesn’t give a gift.

Well one way to handle this situation would be to set aside fifty dollars each month for gifts. You can then make your way to the registered store and buy some fabulous gift with all that money. OR, you can get creative and still give a fabulous gift, but do it in a way that doesn’t break the bank.

My solution is to come up with meaningful, creative, and fun gifts that are easy, generic, and cheap. Over the next few posts, I will be sharing my ideas for wedding, birthday, and baby shower gifts that fit this bill – and guarantee a few extra bills in your bank account.

Philip and I are a young married couple, freshly out of college, with tons of friends getting married and popping out babies right and left. On top of our own monthly expenses, we can’t really afford to fork out thirty or forty bucks for a nice gift every time we get a wedding, baby shower, or birthday party invitation. But we also don’t want to be that couple that doesn’t give a gift.

Well one way to handle this situation would be to set aside fifty dollars each month for gifts. You can then make your way to the registered store and buy some fabulous gift with all that money. OR, you can get creative and still give a fabulous gift, but do it in a way that doesn’t break the bank.

My solution is to come up with meaningful, creative, and fun gifts that are easy, generic, and cheap. Over the next few posts, I will be sharing my ideas for wedding, birthday, and baby shower gifts that fit this bill – and guarantee a few extra bills in your bank account.

Share To:

Feb 8, 2010

Why Live Frugally Now? Part 1 (Janssen)

On Friday, when my mom wrote about living on less, someone commented, "My husband and I have a hard time understanding the benefit of suffering now to be wealthy when we are 80. What is the use? I need valid reasons."

I think this is a terrific question; after all, it is pretty difficult to be frugal for the sake of being frugal. There has to be a reason to make the effort and some potential payoff that makes the present lifestyle worth it.

I'm all with her; I don't want to wait until I'm 80 to be wealthy, either! I hope that within 15 years Bart and I can own a home outright, have all our vehicles paid for, have a fully-funded emergency fund, a very full 401(k), and plenty of savings.

And, just as importantly, I don't want to suffer now. Like many of you (dare I say most of you), suffering doesn't really appeal to me. Therefore, I want my frugal lifestyle to not come at the cost of any happiness in the present. I don't want to take no vacations for the next twenty years. I don't want to wear only clothing from Goodwill. I don't want to never go out to dinner. I don't want to live in a tent in my parents' backyard (and I'm fairly sure they don't want me there either).

So then, what is the use? I'll give several reasons, over the course of several posts, why I live frugally, why I think some sacrifice now is going to be worth it later, and how frugality doesn't have to equal suffering.

I think this is a terrific question; after all, it is pretty difficult to be frugal for the sake of being frugal. There has to be a reason to make the effort and some potential payoff that makes the present lifestyle worth it.

I'm all with her; I don't want to wait until I'm 80 to be wealthy, either! I hope that within 15 years Bart and I can own a home outright, have all our vehicles paid for, have a fully-funded emergency fund, a very full 401(k), and plenty of savings.

And, just as importantly, I don't want to suffer now. Like many of you (dare I say most of you), suffering doesn't really appeal to me. Therefore, I want my frugal lifestyle to not come at the cost of any happiness in the present. I don't want to take no vacations for the next twenty years. I don't want to wear only clothing from Goodwill. I don't want to never go out to dinner. I don't want to live in a tent in my parents' backyard (and I'm fairly sure they don't want me there either).

So then, what is the use? I'll give several reasons, over the course of several posts, why I live frugally, why I think some sacrifice now is going to be worth it later, and how frugality doesn't have to equal suffering.

Share To:

Feb 5, 2010

How Low Can You Go? (Carole)

Over the Christmas holidays, I finally sat down and read The Millionaire Next Door by Thomas Stanley, Ph.D. and William Danko, Ph.D. If you’re old enough, you’ll remember this book was EVERYWHERE back in the late 1990’s. I dutifully bought a copy and it has sat on my bedroom bookshelf ever since.

For whatever reason, December 2009 seemed like the time to finally read it. I don’t quite know what I expected, but I’m sure I thought it would be more entertaining to read than it actually turned out to be. However, the information was terrific (even if presented in an amazingly dull fashion) and I kept reading until I finished --and I’ve thought about much of that information every day since. So, a worthwhile book, if you can drag yourself through it.

A quote in the introduction pretty much sums up the book’s message:

“Wealth is not the same as income. If you make a good income each year and spend it all, you are not getting wealthier. You are just living high. Wealth is what you accumulate, not what you spend.”

When we imagine the wealthy in the United States, we tend to think of movie stars or CEO’s of major corporations. These people do obviously exist and they are certainly rich, but it turns out that MOST millionaires in the USA are pretty average people, with pretty average jobs. In fact, you probably know a few millionaires, but have no idea they have the kind of money they do.

According the Drs. Stanley and Danko, the vast majority of millionaires don’t live in exclusive neighborhoods, don’t drive expensive cars or send their children to private schools. In fact, most people who are spending their money on these kinds of things, are living paycheck to paycheck – but trying to fool everyone (including themselves) into thinking that they are rich. Truly wealthy people usually live way below their income level (as much as 30 – 50% below) and invest their money. And they've lived like this for decades, especially when their income was very low in their younger years -- and it made them wealthy.

Can you imagine living on half of your current income? Would it kill you? Probably not. However, most of us (without having to actually tell anyone) want people to KNOW how much we make. Actually, most of us want others to think we make MUCH MORE than we really do. So we buy things: clothes, cars, purses, houses, 2nd homes, shoes, electronics, phones, CDs, furniture, dinner out, and vacations to exotic places like we are Paris Hilton or one of Bill Gates’ children (no relation J). And we fritter away our current income and our wealthy financial future -- all for pride.

In the coming weeks, I’m going to share some ideas for living WAY BELOW your income level. It’s one of your most important steps to becoming very wealthy.

Share To:

Feb 4, 2010

Only Spending One Dollar (Merrick)

If you go to Smiths for your groceries one week and Macey’s the next, you may see prices vary slightly. But overall they’ll be fairly similar. You may go to Chevron one week to fill your car with gas and Conoco the next and the cost per gallon might differ a few cents, but will be fairly parallel. I think this is pretty standard across the board – identical items are priced almost identically no matter where you buy them.

Well I’m going to let you in on a secret that will change your life. If you go to the Dollar Store, this is NOT the case. Items are only a dollar compared to their outrageously priced twin sold at another store!

No, I do not shop at the Dollar Store for everything. But there are several items that I will never buy at other stores because their prices are such a rip-off.

1. Wrapping Paper: We have all bought wrapping paper and know how expensive it is! You spend $4-5 on a skimpy roll that will wrap only three gifts. And if you want something with more than a yard of paper on the roll, you end up forking over close to $10!

2. Greeting Cards: If you go to Hallmark, Walmart, the grocery store, or anywhere else that sells greeting cards, you better plan on spending anywhere from $3-6. The Dollar Store? Every single card is 2 for $1.

3. Ribbon: They sell those big spools of curling ribbon for $1, and also wired holiday ribbon for $1; both very good deals.

There are more great deals at the dollar store, but in my opinion these are three of the best and among the purchases that I make most frequently.

So next time you have a baby shower, wedding or birthday party to attend, spend your money on the gift; not the wrapping. Go to the Dollar Store and be amazed by their outrageously low prices.

Well I’m going to let you in on a secret that will change your life. If you go to the Dollar Store, this is NOT the case. Items are only a dollar compared to their outrageously priced twin sold at another store!

No, I do not shop at the Dollar Store for everything. But there are several items that I will never buy at other stores because their prices are such a rip-off.

1. Wrapping Paper: We have all bought wrapping paper and know how expensive it is! You spend $4-5 on a skimpy roll that will wrap only three gifts. And if you want something with more than a yard of paper on the roll, you end up forking over close to $10!

2. Greeting Cards: If you go to Hallmark, Walmart, the grocery store, or anywhere else that sells greeting cards, you better plan on spending anywhere from $3-6. The Dollar Store? Every single card is 2 for $1.

3. Ribbon: They sell those big spools of curling ribbon for $1, and also wired holiday ribbon for $1; both very good deals.

There are more great deals at the dollar store, but in my opinion these are three of the best and among the purchases that I make most frequently.

So next time you have a baby shower, wedding or birthday party to attend, spend your money on the gift; not the wrapping. Go to the Dollar Store and be amazed by their outrageously low prices.

Share To:

Feb 3, 2010

Mint.com - Part 3 (Janssen)

And here's the part it seems like everyone has been waiting for. . .the transactions tab! Duhn, duhn, duhn.

If you have mint.com attached to your accounts, it'll pull in all your transactions every time you log in. No effort. Brilliant.

So here is a (much-edited for privacy) view of our transactions tab. You'll see the date of the purchase, the description of the transaction (or name of the business), the category, and the amount of the transaction. If it was a transaction where you spent money, the amount is in black. If it's a transaction where you made money, it's in green (as you'll notice in our extremely high interest income deposits of . . .about four dollars).

So here is a (much-edited for privacy) view of our transactions tab. You'll see the date of the purchase, the description of the transaction (or name of the business), the category, and the amount of the transaction. If it was a transaction where you spent money, the amount is in black. If it's a transaction where you made money, it's in green (as you'll notice in our extremely high interest income deposits of . . .about four dollars).

We sit down every Sunday as part of our Family Home Evening and review our transactions for the week, making changes as needed.

For example, you'll see two payments to Parkway Auto, both in the category of "Service and Parts." Except only one of them was an oil change. The other one was a tank of gas. Not "Service and Parts." (I've circled it in red below).

If you click on the transaction, a little gray tab marked "Edit Details" will appear:

Click "Edit Details," and this screen will drop down on top of your transactions.

If you click "Service & Parts" as the category, you'll get a drop-down menu of all the possible categories (and you can also add your own):

Staying in the "Auto and Transport," I selected "Gas and Fuel" instead of "Service and Parts" so that it will now accurately reflect that spending in our gas budget (back in our budget/planning tab).

Now, if we were only ever getting gas at this location, when I make the category change, it will ask me if I want to create a rule that always names transactions from this location as "Gas and Fuel." I've never bought gas at this place and probably won't again, since their gas is a little more pricey, so I didn't click the checkbox (see an example below).

But sometimes, that making a rule is very helpful. For instance, Bart rides the T into work on occasion. Payments to that account show up as "Subway" on our transaction list. Except, mint.com thinks Subway is the sandwich shop and puts it in the food category. Wrong. The first time I changed it, I checked it when it asked me about the rule and now, as you'll see below, it always categorizes "Subway" as "Public Transportation."

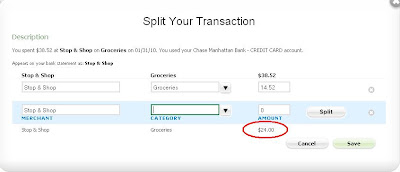

Another thing several people asked about was splitting up transactions. That is to say, if you go to the grocery store and most of your purchase goes into the groceries category but you also have $10 worth of school supplies, can you get Mint to reflect that? You betcha.

Open the transaction you want to fix by selecting it and clicking "Edit Details" (just like before) and then click the handy "Split" button:

This screen will pop up.

Put in the category you want and then the amount of money that belongs in that category and push "Split."

Put in the category you want and then the amount of money that belongs in that category and push "Split."

Now you'll see the first category is $14.52 in groceries. At the bottom (I've circled it), it will show you how much of the total transaction is left (yippee! no math!) and you can add the next category and the amount spent there. If you need a third category, push "Split" again. If not, push "Save" and ta-da. Split.

Now you'll see the first category is $14.52 in groceries. At the bottom (I've circled it), it will show you how much of the total transaction is left (yippee! no math!) and you can add the next category and the amount spent there. If you need a third category, push "Split" again. If not, push "Save" and ta-da. Split.

One other question that got asked. Someone asked if they could hide where money was spent if they were trying to surprise a spouse or something. Absolutely. Just click on your transaction you want to rename, highlight the name of the place you bought whatever it was and type something different in, like "DO NOT LOOK ON PAIN OF DEATH:"

And then recategorize it as something like "Gifts" or whatever your category is for spending on another person. Otherwise "DO NOT LOOK ON PAIN OF DEATH" won't be very effective if they can see "Electronics and Games" as the category right next to it.

And then recategorize it as something like "Gifts" or whatever your category is for spending on another person. Otherwise "DO NOT LOOK ON PAIN OF DEATH" won't be very effective if they can see "Electronics and Games" as the category right next to it.

Any other questions? I am happy to bombard you with screen shots!

If you have mint.com attached to your accounts, it'll pull in all your transactions every time you log in. No effort. Brilliant.

We sit down every Sunday as part of our Family Home Evening and review our transactions for the week, making changes as needed.

For example, you'll see two payments to Parkway Auto, both in the category of "Service and Parts." Except only one of them was an oil change. The other one was a tank of gas. Not "Service and Parts." (I've circled it in red below).

If you click on the transaction, a little gray tab marked "Edit Details" will appear:

Click "Edit Details," and this screen will drop down on top of your transactions.

If you click "Service & Parts" as the category, you'll get a drop-down menu of all the possible categories (and you can also add your own):

Staying in the "Auto and Transport," I selected "Gas and Fuel" instead of "Service and Parts" so that it will now accurately reflect that spending in our gas budget (back in our budget/planning tab).

Now, if we were only ever getting gas at this location, when I make the category change, it will ask me if I want to create a rule that always names transactions from this location as "Gas and Fuel." I've never bought gas at this place and probably won't again, since their gas is a little more pricey, so I didn't click the checkbox (see an example below).

But sometimes, that making a rule is very helpful. For instance, Bart rides the T into work on occasion. Payments to that account show up as "Subway" on our transaction list. Except, mint.com thinks Subway is the sandwich shop and puts it in the food category. Wrong. The first time I changed it, I checked it when it asked me about the rule and now, as you'll see below, it always categorizes "Subway" as "Public Transportation."

Another thing several people asked about was splitting up transactions. That is to say, if you go to the grocery store and most of your purchase goes into the groceries category but you also have $10 worth of school supplies, can you get Mint to reflect that? You betcha.

Open the transaction you want to fix by selecting it and clicking "Edit Details" (just like before) and then click the handy "Split" button:

This screen will pop up.

One other question that got asked. Someone asked if they could hide where money was spent if they were trying to surprise a spouse or something. Absolutely. Just click on your transaction you want to rename, highlight the name of the place you bought whatever it was and type something different in, like "DO NOT LOOK ON PAIN OF DEATH:"

Any other questions? I am happy to bombard you with screen shots!

Share To:

Feb 2, 2010

The Third of 3 Little Budget Secrets (Carole)

The final budgeting secret is to SWEEP! Huh??

Let me explain. After you’ve finished paying all your regular monthly bills, and also transferred the money to your savings account to cover your occasional bills that you’re saving up for -- then take ALL THE REST of the money in your checking account (except what the bank demands you keep in the account to keep it open) and SWEEP it into your savings account.

Add one more sub-account in your lovely savings account and call it your Rainy Day Fund. This “swept” money goes in this fund. The money in this new fund accomplishes two important goals in keeping you on your budget:

- It removes the money from your checking account where it is EASY to spend, and tucks it away in your savings account where it is HARDER to spend. And. . .

- It gradually grows a fat cushion between you and a financial emergency.

Most financial experts recommend that you work toward having at least $1,000 in this Rainy Day Fund. But keep going. The ultimate goal would be to have about 6 months worth of household EXPENSES (not gross income) saved in there. That ends up being quite a few thousand dollars! This money is not to buy a new blender or TV or a new car. It is to pay the bill when the washing machine suddenly dies, or when your car engine blows up or you lose your job. Those small or large money emergencies that kill your budget!

Make the $1,000 your first goal, and then work toward having one month’s worth of expenses, then two months and so on. You will feel safer than you have ever felt before.

So, SWEEP your checking account --it’s the easiest way to keep your monthly budget healthy and safe.

Share To:

Feb 1, 2010

Are you Getting Paid to Shop? (Merrick)

Are you one of those people who never makes an online purchase without checking for free shipping codes, or a 10% off coupon? Well, I am totally one of those people. But it seems like whenever I search for coupon codes or discounts, either I can’t find any, or there are a few great ones but they have all expired. Then I end up having to pay full price and it makes me mad.

Then I discovered Ebates.com. Do you know about this glorious website? If you don’t, go there right now and check it out.

Ebates is not only great because it has access to tons of great online coupons, but it’s mostly great because it pays you to shop online. Seriously. Once you sign up (which is free), you can search through hundreds of stores, where it shows you what percentage of your total order they will give back – anywhere from 1% to 25%, depending on the store!

Just browse through their list until you find the store you want to order from, and then click on their “Shop Now” button, where it will automatically connect you to that store’s website. Do your shopping as normal, and within 2-3 days you can check your ebates account and see the money that has been deposited in your account. From there, you can choose to have your money sent to you via paypal or check, and every three months that money is automatically sent to you (as long as you have more than $5 in your ebates account. Otherwise it sits there until you accumulate $5).

How can you go wrong with a site like this? It’s like having a rebate for every single online purchase that you make, which is especially great for purchases you were already planning to make (I’m not encouraging shopping sprees – we are trying to become “frugal wives,” after all).

And finally, if you sign up and then tell your friends about it and they sign up and put your name as their referral, Ebates will give you $5 per friend. [My email address is amerricka72@gmail.com. Just sayin’].

Now head on over to ebates.com and start getting paid to shop!

Then I discovered Ebates.com. Do you know about this glorious website? If you don’t, go there right now and check it out.

Ebates is not only great because it has access to tons of great online coupons, but it’s mostly great because it pays you to shop online. Seriously. Once you sign up (which is free), you can search through hundreds of stores, where it shows you what percentage of your total order they will give back – anywhere from 1% to 25%, depending on the store!

Just browse through their list until you find the store you want to order from, and then click on their “Shop Now” button, where it will automatically connect you to that store’s website. Do your shopping as normal, and within 2-3 days you can check your ebates account and see the money that has been deposited in your account. From there, you can choose to have your money sent to you via paypal or check, and every three months that money is automatically sent to you (as long as you have more than $5 in your ebates account. Otherwise it sits there until you accumulate $5).

How can you go wrong with a site like this? It’s like having a rebate for every single online purchase that you make, which is especially great for purchases you were already planning to make (I’m not encouraging shopping sprees – we are trying to become “frugal wives,” after all).

And finally, if you sign up and then tell your friends about it and they sign up and put your name as their referral, Ebates will give you $5 per friend. [My email address is amerricka72@gmail.com. Just sayin’].

Now head on over to ebates.com and start getting paid to shop!

Share To: